Written by

Written by  Edited by

Edited by

If you’re looking for a financial advisor, Form ADV is an essential point of reference. In fact, this publicly available paperwork must be filed with the U.S. Securities and Exchange Commission (SEC) by all financial advisor firms with more than $25 million in AUM. Form ADV includes dozens of pages of information about a firm. This includes its fee structure, total assets under management, other business activities, any disciplinary issues on record and more.

A financial advisor can help you with retirement and estate planning, investment portfolios, taxes, and more.

What Is Form ADV?

Form ADV is officially called the Uniform Application for Investment Adviser Registration and Report by Exempt Reporting Adviser. Any investment advisor that manages more than $25 million must submit this registration document to the U.S. Securities and Exchange Commission and to state regulators. Registered advisors must update their Form ADV annually.

Form ADV includes two parts, both of which provide detailed information about the firm. Part I is a fill-in-the-blank form, and Part II is a brochure written in prose. The first part contains basic facts about the firm, like its fees, client types, assets under management and any disclosures. The second part explains its services, investing approach and any conflicts of interest. Think of it as a firm’s backstory.

Form ADV provides a wealth of information about registered firms. Potential clients should always review a firm’s Form ADV before they begin to work with the firm.

The SEC paperwork provides information that most firms don’t disclose on their websites. This includes whether they have any disclosures, charge performance-based fees, or earn commissions from selling products to clients. It may not always be clear when a firm last updated its website, but firms must update Form ADV annually.

Breaking Down Form ADV Part I

As mentioned before, Part I of Form ADV is a fill-in-the-blank form. It can range from 15 pages to over 100, depending on the firm’s disclosures.

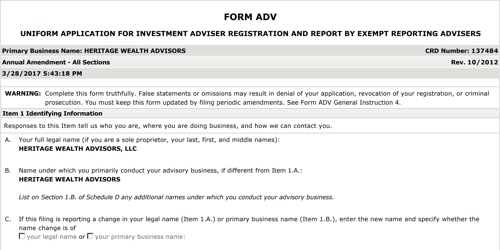

Form ADV Part I is divided into at least 12 items. The first section establishes basic information about a firm. You’ll find things like its legal name, the name it does business under, its address, website, and phone number.

Items 3 through 7 provide a wealth of information for prospective clients. This is where the firm lists:

- Total assets under management

- Total number of accounts

- Number of employees serving in an advisory function

- Percentages of each client type it serves (including individuals versus high-net-worth individuals)

- Compensation arrangements (the financial advisor fees it charges for services)

- Advisory activities (whether it provides financial planning, portfolio management, etc.)

- Other business activities (whether it’s also an insurance broker or broker-dealer)

Another notable section of the Form ADV Part I is Item 11. In this section, the firm reveals whether it has any disclosures on its record. If it does, the firm must state what its offenses were and whether any supervised persons were involved. The firm must also attach a report that provides further detail on any affirmative response. 1

Breaking Down Form ADV Part II

The SEC often labels this part of Form ADV as “Part 2 Brochures.” Part II of Form ADV contains a table of contents, which makes it easier to navigate than Part I.

Like the first part, Part II is divided into various items, with 18 items in total.

Part II: Items 1-8

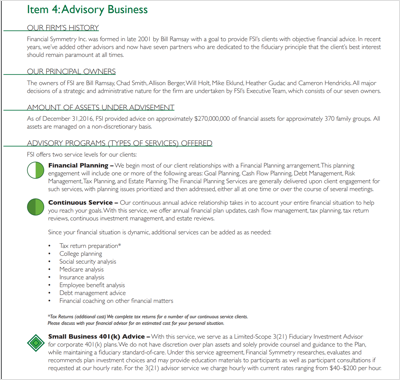

The first eight items of Form ADV Part II typically contain the most relevant information for prospective clients. The first few items include the cover page, any changes that have occurred since the firm’s last filing, and the table of contents. The true beginning of Part II is Item 4, which offers an overview of the firm. This is where you can find the firm’s founding year, its owners, and the services it provides.

Items 5 and 6 cover the firm’s fees. Item 5 outlines the exact fees a firm charges for its various services. Item 6 makes clear whether the firm charges performance-based fees or offers side-by-side management.

A particularly important item to consider is Item 7, where the firm describes its typical clients and often lists its account minimum. Item 8 provides a deep dive into the firm’s methods of analysis and investment strategies, as well as a warning of the risks involved with investing. This is where you can gain a better understanding of how the firm invests its clients’ assets and what investment types it typically uses.

Part II: Items 9-18

These items provide information about the firm’s inner workings and policies. Item 9 provides more details on any disciplinary information, while Item 10 discloses any other financial industry activities and affiliations. You can usually find out in Item 10 whether a firm earns commissions from selling insurance products or securities.

Item 11 is the firm’s code of ethics and Item 12 details a firm’s brokerage practices. The remaining sections outline a firm’s policies on account reviews, client referrals, custody of clients’ assets, voting client securities and any other relevant financial information. 2

How to Access a Firm’s Form ADV

Form ADV is publicly available through the SEC’s Investment Advisor Public Disclosure website. On this website, you can search for individual advisors and advisory firms by either the firm or advisor’s name or their Central Registration Depository (CRD) number. The SEC assigns this number to every registered representative licensed to sell securities in the U.S. CRD stands for Central Registration Depository, a database that contains information about firms and brokers.

Many firms also provide a link to their Form ADV on their websites. Any registered representative should be able to produce a copy of this paperwork if you request it.

What to Look for When You Pull a Firm’s Form ADV

Once you have the form in front of you, the disclosure history is a good place to start. Every firm must report whether it or any of its advisors have faced regulatory actions, arbitration proceedings or client complaints. A single resolved matter from years ago looks different than a pattern of recurring issues. The specifics tell you more than the presence or absence of a disclosure alone, so read what actually happened before drawing conclusions.

The compensation section is worth your time because it shows you every way the firm gets paid. Some firms charge a percentage of assets. Others bill hourly, collect flat retainers or earn commissions on the products they recommend. A firm that collects fees from you and commissions from product providers has a built-in tension that you should understand before signing on. That doesn’t make the firm dishonest, but it does mean you should ask how it decides when to recommend a commissioned product over one that doesn’t pay the firm anything extra.

Client Data and Strategy

The form breaks down the firm’s client base by category, showing what percentage are individuals, high-net-worth investors, institutional clients or retirement plans. This tells you whether you’re the type of client the firm is built to serve. A firm where 85% of accounts belong to institutional investors may not have the infrastructure or interest to give a retail client with a $400,000 investment portfolio the attention they expect. Knowing where you fit in the client mix before your first meeting saves everyone time.

You can also calculate a rough client-to-advisor ratio from the numbers reported in the form. Total accounts divided by advisory employees gives you a sense of how stretched the team is. A firm managing 4,000 accounts with six advisors is running a volume practice, which often means standardized portfolios and limited customization. That model works well for some people and poorly for others, but the form gives you the data to know what you’re walking into.

The investment strategy section describes how the firm manages money, what types of securities it favors and how it thinks about risk. If you have strong feelings about active versus passive management, alternative investments or concentrated stock positions, this is where you find out whether the firm’s approach matches yours. Reading this section before an introductory call means you spend less time on basics and more time on the questions that actually matter to your decision.

What Form ADV Doesn’t Tell You

While Form ADV provides transparency on an advisor’s fees, conflicts of interest, and regulatory history, it has limitations. It doesn’t always reveal an advisor’s investment philosophy, client service approach or communication style – factors that can significantly impact a client’s experience. Additionally, while disciplinary disclosures are included, they may lack context, making it difficult to assess the severity of past infractions.

Consumers should supplement Form ADV with additional research. Reading client reviews, asking about real-life case studies and conducting interviews can provide insight into an advisor’s approach. Requesting a sample financial plan or discussing how they tailor strategies to different client needs can also help.

Since Form ADV doesn’t highlight ongoing service commitments, prospective clients should clarify how frequently an advisor communicates, whether they proactively adjust strategies, and how they handle market downturns.

Tips for Reading Form ADV

Form ADV contains valuable details, but knowing where to focus can make reviewing it more effective.

Start with Part 2, which is written in plain language and outlines the advisor’s services, fees, and conflicts of interest. Pay attention to Item 5, which explains how the advisor charges clients—whether through a flat fee, hourly rate, or percentage of assets under management (AUM).

Next, check Item 9 for any disciplinary disclosures, but research further to understand the severity and context. In Item 10, look for affiliations with other financial firms, which could indicate potential conflicts of interest.

Part 1, while more technical, provides details on assets under management and ownership structure, which can help assess the firm’s stability.

Top Financial Advisors By City and State

If you’re interested in the information within Form ADV and want to choose a financial advisor based on it without having to read through the form yourself, consider using our top Financial Advisors tool. This will enable you to sort by city and state to find financial advisors who serve your area and who have a clean record. You can even find a financial advisor that specializes in the service you need the most.

Bottom Line

Form ADVs are available through the SEC and remain some of the most valuable resources for investors. They allow you to learn about a firm’s services, fees and investment strategies. This can, in turn, make you infinitely more comfortable when choosing a firm to invest your money with.

Tips for Choosing a Financial Advisor

- There are many different financial advisors you can work with, and that can make choosing one quite difficult. SmartAsset’s free tool matches you with financial advisors who serve your area, and you can have a free introductory call with your advisor matches to decide which one you feel is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

- Any firm that registers with the SEC must abide by fiduciary duty, which means it must act in clients’ best interests at all times. Therefore, looking for a fiduciary financial advisor is extremely important.

- Try to find an advisor who has certifications to their name. A certified financial planner (CFP) is one of the most prestigious designations and requires extensive experience and effort to obtain.

Photo credit: ©iStock.com/JohnnyGreig, https://adviserinfo.sec.gov/

Article Sources

All articles are reviewed and updated by SmartAsset’s fact-checkers for accuracy. Visit our Editorial Policy for more details on our overall journalistic standards.

- Securities and Exchange Commission. https://www.sec.gov/files/formadv-part1a_1.pdf. Accessed 16 Apr. 2026.

- Securities and Exchange Commission. https://www.sec.gov/files/formadv-part2_0.pdf. Accessed 16 Apr. 2026.