Written by

Written by  The costs of long-term care for older adults can be significant, and federal Medicare health insurance benefits do not cover most of these costs. Most people who incur costs for long-term care cover them with a combination of personal savings, long-term care insurance and Medicaid, among other sources. Consider working with a financial advisor as you find ways to pay for long-term care needs.

The costs of long-term care for older adults can be significant, and federal Medicare health insurance benefits do not cover most of these costs. Most people who incur costs for long-term care cover them with a combination of personal savings, long-term care insurance and Medicaid, among other sources. Consider working with a financial advisor as you find ways to pay for long-term care needs.

Costs of Long-Term Care

The average semi-private room in a nursing home cost $6,844 per month in 2016, according to the U.S. Department of Health and Human Services’ Administration for Community Living. A private room averaged $7,698 per month. Assisted living facilities typically cost $3,628 monthly. Home health aides went for $20.50 an hour and a day in an adult day healthcare center ran $68.

While long-term care insurance can be a good way to pay for long-term care costs, not just anyone can buy a policy. Long-term care insurance companies won’t sell coverage to people already in long-term care or having trouble with activities of daily living. They may also refuse coverage if you have had a stroke or been diagnosed with Alzheimer’s disease or other forms of dementia, cancer, AIDS or Parkinson’s Disease. Even healthy people over 85 may not be able to get long-term care coverage.

Paying for Long-Term Care

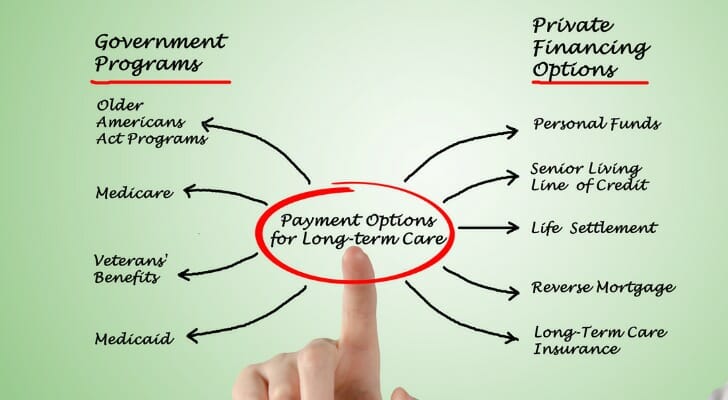

The potential costs of long-term care be challenge for even a relatively prosperous patient in the event of an extended stay in a nursing home. However, there are many options for covering these expenses. Some of the major approaches include:

- Federal and state governments – Although the federal government’s health insurance plan doesn’t cover most long-term care costs, it will if pay for up to 100 days in a nursing home if patients required skilled services and rehabilitative care. Similarly, skilled home health or other skilled in-home service may be covered by Medicare. Sometimes state programs that will pay for long-term care services for people whose incomes are below a certain level and meet other eligibility requirements.

- Private health insurance – Employer-sponsored health plans and other private health insurance will, like Medicare, cover some long-term care costs. Shorter-term, medically necessary skilled care is more likely to be covered.

- Long-term care insurance – Private long-term care insurance policies can cover many of the costs of long-term care. However, policies are not cheap.

- Private savings – Older adults who need long-term care that is not covered by government programs and who don’t have long-term care insurance can use money from their retirement accounts, personal savings, brokerage accounts and other sources.

- Health savings accounts – Funds in these tax-advantaged savings can be withdrawn tax-free to pay for qualifying medical expenses, including those for long-term care. Only people in high-deductible health plans can put money into health savings accounts, however.

- Home equity loans – Many older adults have paid off their mortgages or have significant equity built up in their homes. Home equity loans represent one way to tap this value to pay for long-term care.

- Reverse mortgages – These types of mortgages let homeowners get what amount to home equity loans without having to pay interest or principal on the loans while they are alive. When the homeowner dies or moves out, the entire balance of the loan becomes due. Often when that happens, the lender takes over ownership of the home.

- Life insurance – Asset-based long-term care insurance is a kind of whole life insurance that lets a policyholder use the death benefits to pay for long-term care. Life insurance can also be bought with a long-term care rider as a secondary benefit.

- Hybrid insurance policies – Some long-term care insurance is set up as an annuity. In many of these cases there is a single premium payment, and the insurer will provide benefits that can be used for long-term care costs. You can also buy a deferred long-term care annuity that is specially designed to cover these costs. Alternatively, some permanent life insurance policies have long-term care riders.

Long-Term Care Cost Caveat

While long-term care can be costly, most people will not face extremely burdensome long-term care costs. That’s partly because nursing home stays tend to be short and for a somewhat grim reason: One study by University of California researchers found most people died within six months of entering a nursing home.

Also, the overwhelming majority of elder adults are not in nursing homes and many never go into them. For instance, in 2016, according to the Centers for Disease Control, there were nearly 48 million adults 65 and older, of which only 1.3 million were living in nursing homes.

The Bottom Line

While paying for long-term care costs can seem daunting, people have many sources for funds to cover these expenses. Sources include Medicare, Medicaid, long-term care insurance, private savings, home equity and life insurance.

While paying for long-term care costs can seem daunting, people have many sources for funds to cover these expenses. Sources include Medicare, Medicaid, long-term care insurance, private savings, home equity and life insurance.

Tips on Funding Long-Term Care

- The multitude of options for paying for long-term care means this decision is best made with the assistances of an experience and qualified financial advisors. Finding a qualified financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three financial advisors in your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

- Use our free retirement calculator to get a quick estimate of how you’re doing preparing for life after work.

Photo credit: ©iStock.com/FatCamera, ©iStock.com/vaeenma, ©iStock.com/kazuma seki