Written by

Written by  Edited by

Edited by  Edited by

Edited by

IRS Form W-4 tells your employer how much federal income tax to withhold from your paycheck. You’ll be asked to fill one out when you start a new job. You can also submit a new W-4 to your payroll department when you have a life event that affects your taxes like getting married or having a baby, or if you paid too little or too much in taxes. The form used to be a bit complicated, but the IRS simplified it for 2020 and beyond. Now there are only five steps, three of which you can skip if you are the only breadwinner in your family, have only one job and have no dependents. The two mandatory steps involve providing your name, address, Social Security number, filing status and signature.

A financial advisor can help optimize your financial plan to lower your tax liability.

What Is Form W-4?

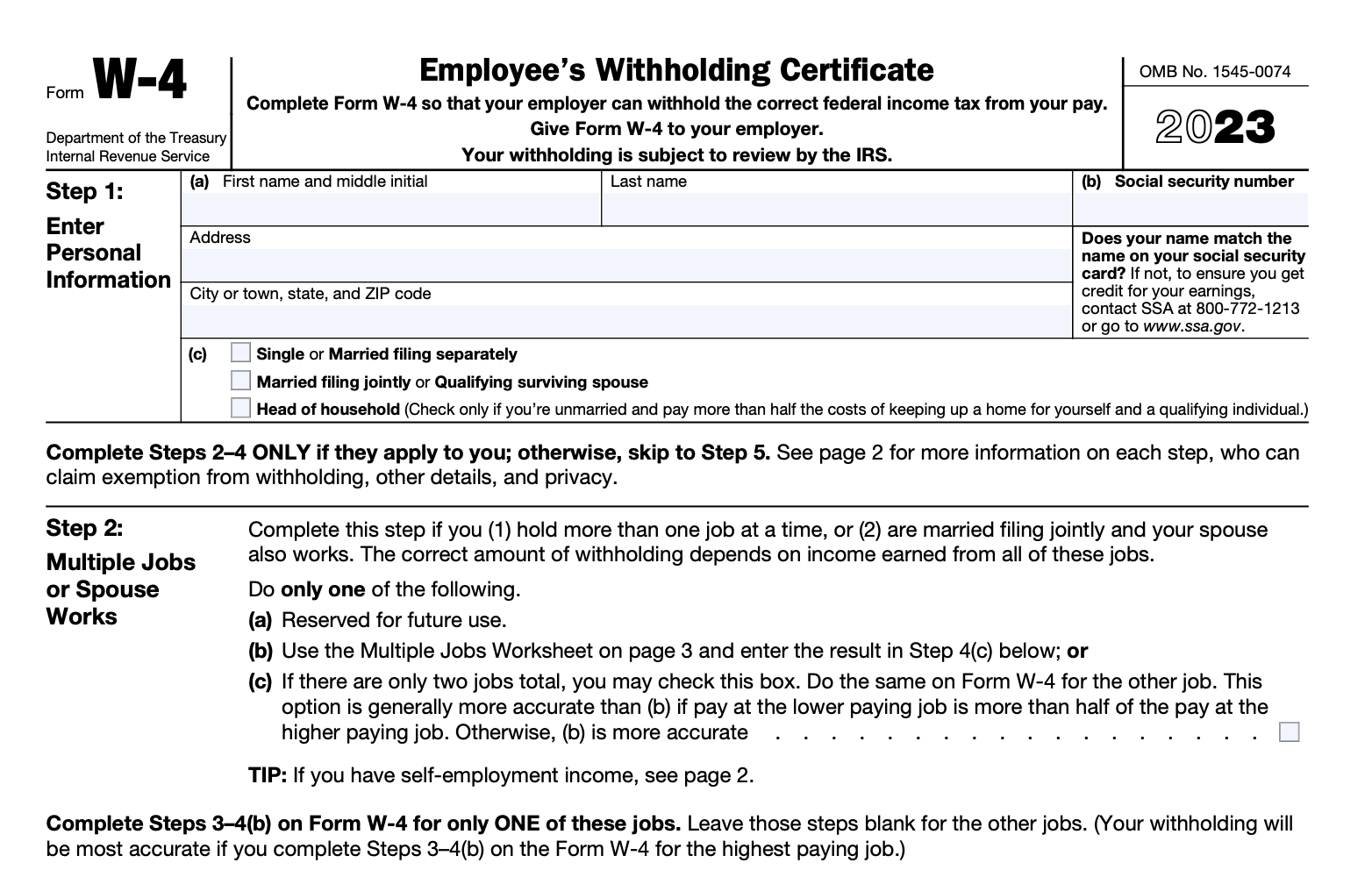

The official title of Form W-4 is Employee’s Withholding Certificate. When you complete the W-4 correctly, it informs your employer of how much money to withhold from your paycheck for federal income taxes. Because of this, you need to fill out a new copy of the form anytime you start a new job.

As noted earlier, you should also fill out a new W-4 if you get married or divorced, have a child, start a side hustle or paid too little or too much in taxes. The IRS actually recommends filling out a new W-4 each calendar year to ensure that you’re paying the right amount in taxes. But if your income and taxes remain the same, you likely don’t need to.

What’s on Form W-4?

Form W-4 comes in a four-page packet. However, the form itself is just one page and has only five steps. In Step 1, you are asked to provide your:

- Name and address

- Social Security number

- Filing status – single, married or married filing separately

Steps 2 through 4 are optional and only apply to taxpayers who have multiple jobs or a working spouse (Step 2), are claiming dependents (Step 3), or who have special adjustments to their income, deductions or withholding (Step 4). Step 5 is signing the form.

Employers then enter their name, address, employer identification number (EIN) and the first date of the employee’s employment. The other three pages of the W-4 packet include instructions and the two-earners/multiple jobs worksheet and the tax table.

What Is Federal Tax Withholding?

Each time you get paid, your employer takes out (withholds) a certain amount of money from your paycheck. This money goes toward your federal income taxes and some other federal taxes, like the FICA taxes. Because the U.S. has a pay-as-you-go tax system, you pay your income taxes throughout the year instead of as one lump sum during tax season. So every employer needs to withhold money for their employees’ federal taxes and send it to the IRS. When determining how much to withhold, your employer will consider your salary and the information on your W-4.

It’s also good to note that retirees who receive a monthly pension or annuity check must also withhold money from each payment. If you have other earnings, such as from bonuses, commissions or gambling, you likely need to increase your withholding. Self-employed workers, independent contractors, small business owners and others without an employer pay quarterly estimated taxes.

Estimating your withholding ahead of time can help you avoid owing a large balance or receiving an unexpectedly small refund at tax time. Our income tax calculator can help you see how your income, withholding and other earnings may affect your overall tax liability for the year.

What Are Other Adjustments on the W-4?

When your employer withholds tax, your salary will factor in because it determines your tax bracket. However, you can change the exact amount your employer withholds by listing other income and deductions.

Additionally, you can direct your employer to withhold a certain extra amount. This additional withholding goes toward your income taxes and helps you right-size your taxes so that you aren’t underpaying over the year. Ideally, you’ll neither owe a significant amount of money nor get a big refund when you file your tax return in April.

For example, let’s say you estimate your federal tax return and find that you will owe $1,000 at tax time. If you get paid twice each month (24 pay periods) then you may want to withhold an additional $40 from each paycheck. This will bring you close to paying how much you owe in annual income taxes so you don’t owe extra.

What If an Employee Doesn’t Submit a W-4?

Employers need current W-4s to withhold the correct amount of federal income taxes for employees. If an employee does not complete and sign a W-4, the IRS requires the employer to withhold taxes at the highest withholding rate possible.

Bottom Line

The Form W-4 tells your employer how much money to withhold from your paycheck for federal income taxes. You need to fill out a W-4 anytime you start a new job. You should also update the form when you experience major changes that affect your taxes, like when you marry or have a child. The streamlined form has only five steps total, and many taxpayers won’t need to worry about steps 2 through 4.

Tax Planning and Your Financial Plan

- Taxes are just one aspect of your financial situation. To build a financial plan that accounts for taxes and other factors, it’s a good idea to work with a financial advisor. Finding one doesn’t have to be hard. SmartAsset’s free tool matches you with vetted financial advisors who serve your area, and you can have a free introductory call with your advisor matches to decide which one you feel is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

- If you have a side hustle, you’ll need to pay taxes on that extra income. You can do that by either paying quarterly estimated taxes or by having more withheld from your paycheck. To get a sense of how much to withhold, use our federal income tax calculator. (You’ll need a pay stub to see how much you are paying in taxes and how much more you owe.)

Photo credit: IRS.gov, ©iStock.com/mediaphotos, ©iStock.com/PeopleImages