Written by

Written by  Edited by

Edited by  Edited by

Edited by  Reviewed by

Reviewed by

If you give someone cash or property valued at more than the 2026 gift tax exclusion limit of $19,000 ($38,000 for married joint filers), you’ll have to fill out Form 709 for gift tax purposes. But don’t fret. This doesn’t always mean you’ll owe an actual tax. The government requires this to keep track of your lifetime gift and estate tax exemption. It’s only when you use up the large lifetime exemption that you would owe an out-of-pocket tax. Still, filling out Form 709 can get complicated. This article will walk you through the process step-by-step. It’ll also help you determine if you need to fill out Form 709 in the first place.

If you’re looking help with specific areas of your finances, including tax planning, consider speaking with a financial advisor.

What Counts Toward the Gift Tax?

The IRS defines a gift as virtually anything of value that you give to another individual or entity without expecting anything of equal or lesser value in return. It doesn’t have to be cold, hard cash, either. This covers several types of asset and property. That includes a house, car, jewelry and more. It also includes several types of financial accounts such as an investment portfolio.

The following may also be considered gifts:

- A hefty loan you gave someone with zero interest

- Forgiving large debt that’s owed to you

- Gifting money out of retirement accounts

Nonetheless, the government does give you some wiggle room. Giving money to the following individuals or institutions is never considered a taxable gift:

- Spouse who’s a U.S. citizen (if spouse is not a citizen, there is a $194,000 limit)

- Care provider to cover someone else’s qualified medical expenses

- Educational institution to cover tuition only

- Qualified charitable organizations

- Political organizations

So you can give as much as you want to those individuals and institutions for the year without needing to fill out Form 709 or pay a gift tax.

But even if you think you’ve given away a lot in taxable gifts, you may not need to fill out Form 709 or pay a tax. That’s because of the gift tax limits.

What Is the Annual Gift Tax Exclusion?

For tax year 2026, you may give someone cash or property valued at up to $19,000 without needing to fill out Form 709. The exclusion applies per person. So you can give your son, daughter and grandchild $19,000 each without catching Uncle Sam’s attention. For married couples making joint gifts to a third party, the annual exclusion for the 2026 tax year is $38,000.

But once you transfer a taxable gift valued above those limits to any one person, you have to fill out Form 709. Officially, it’s called the United States Gift (and Generation-Skipping Transfer) Tax Return.

If you make a joint gift with your spouse, each individual must fill out a Form 709. There is no joint Form 709.

However, you won’t need to pay an actual tax unless you go beyond your lifetime gift and estate tax exemption. The Trump tax plan, known as the Tax Cuts and Jobs Act (TCJA), raised those limits considerably in 2018. Currently, the lifetime exemption is $15 million per individual for tax year 2026 (up from $13.99 million in 2025).

How to Fill Out Form 709

If you’ve figured out you must fill out Form 709, follow the instructions below.

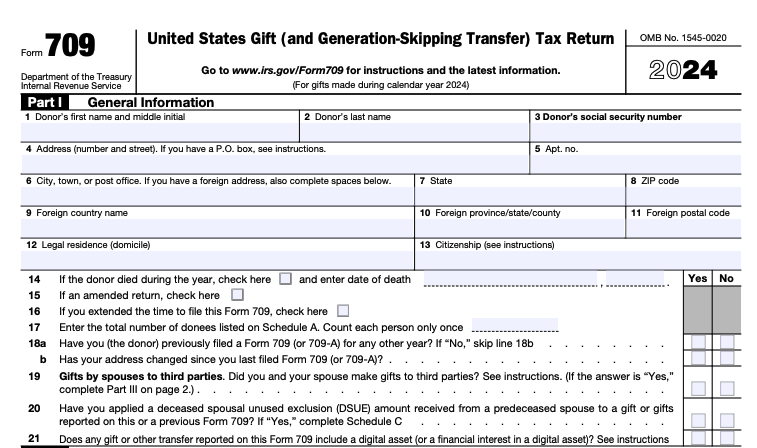

First, complete the General Information section on part one of the form in lines 1 through 13. Line 19 would also allow you to check off on whether you and your spouse made joint gifts for the tax year. If not, you may skip Part III. Note that your spouse must also sign Form 709 in the appropriate spot if you made joint gifts. But each would have to fill out his or her own form.

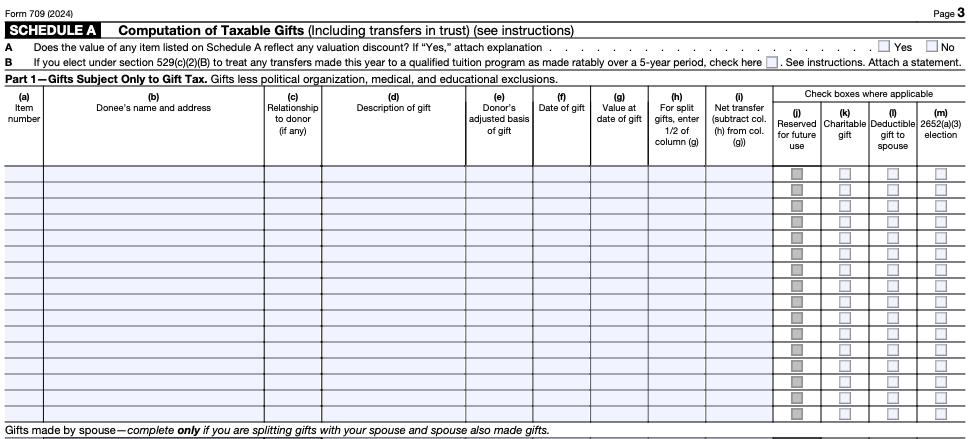

Report the gifts on Schedule A: Computation of Taxable Gifts. Here, you’d provide information such as a description of the gift, the recipient, and its value at the time it was made.

You may also report transfers subject to the gift tax and/or generation-skipping transfer tax if applicable. In addition, you’d report transfers made to trusts if any.

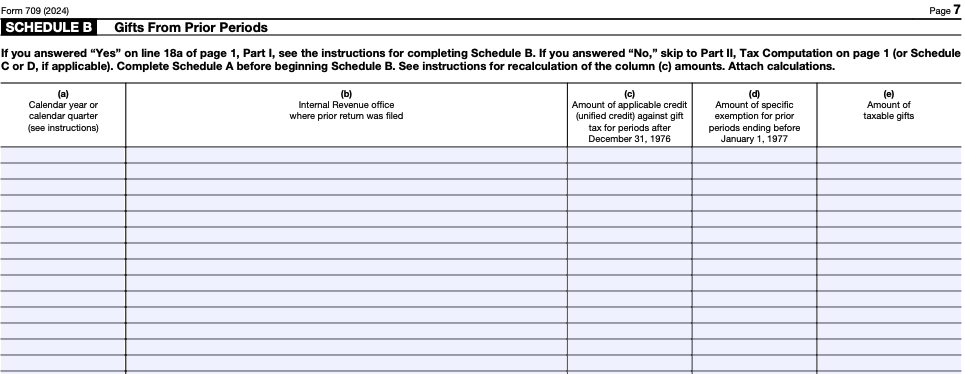

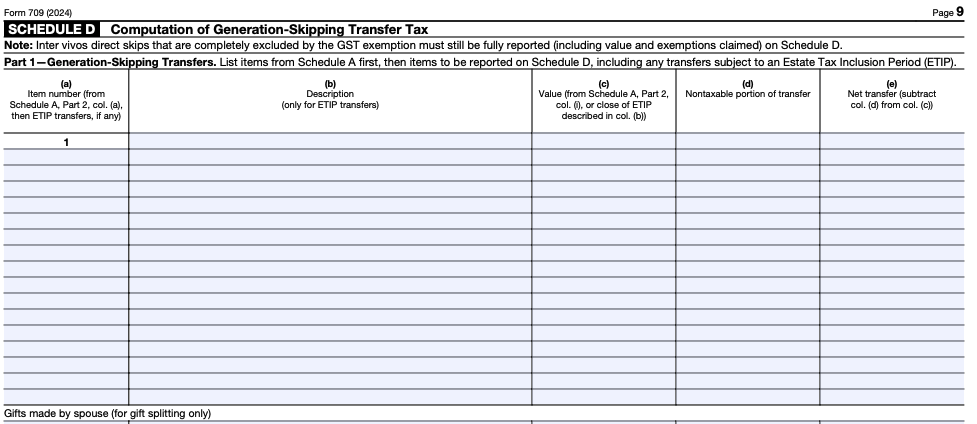

If any applies to you, complete the sections titled Gifts From Prior Periods, Deceased Spousal Unused Exclusion Amount and Computation of Generation Skipping Transfer Tax. These are Schedule B, C, and D, respectively.

Complete Part II, known as “Tax Computation.” It is located on the first page of Form 709. Refer to the “Table for Computing Gift Tax” under instructions to calculate the tax on the amount of reported gift or gifts. You may apply your lifetime gift and estate tax exemption, also known as the unified credit. So you don’t have to pay an out-of-pocket tax if you use this exemption. It will, however, reduce how much you can give and transfer out of your estate tax-free in the future.

Finally, sign and date the form.

Before you file your return, use our income tax calculator to estimate what you may owe or receive.

What Happens to Your Lifetime Exemption After You File

Filing Form 709 does not just report a single gift and move on. It starts a running ledger that the IRS maintains for the rest of your life. Every taxable gift you report gets added to a cumulative total, and that total is measured against your lifetime exemption. The distance between what you have given and the current exemption limit is what you have left to transfer tax-free, either through future gifts or through your estate when you die. Schedule B on the form is where you report gifts from prior years, and each new filing builds on everything that came before it.

Most people who file Form 709 will never come close to using up their full exemption. At $15 million for 2026, the threshold is high enough that the vast majority of filers are simply reporting a gift and moving on with no tax owed. But the amount you use during your lifetime still matters because it directly reduces what your estate can pass tax-free after your death. If you gave away $2 million in taxable gifts over the course of your life, your estate has $13 million of exemption left, not $15 million. For families with estates anywhere near that range, the lifetime total is not a technicality. It is the number that determines whether the estate owes federal tax.

The current exemption is historically high, and there is no guarantee it stays there. Congress has changed the number multiple times over the past two decades, and the possibility of a future reduction is a regular part of the estate planning conversation. If the exemption is lowered down the road, gifts you already made under the higher limit are generally protected under current IRS guidance. But any remaining exemption you were counting on for future gifts or estate transfers could shrink. That means a plan built around today’s number may not work the same way under tomorrow’s rules.

This is why keeping records of every Form 709 you file is more important than most people realize. The IRS expects you to report all prior-period gifts on Schedule B each time you file a new return. If you cannot account for what you reported five or 10 or 20 years ago, reconstructing that information can be time-consuming and expensive. In some cases, the records may not exist anymore if the preparer who filed the original return has since retired or closed their practice. Keeping a copy of every Form 709 along with the supporting documentation is one of the simplest and most valuable habits in estate planning.

Gifting decisions also do not exist in a vacuum. A gift that reduces your taxable estate might also trigger income tax consequences for the recipient, depending on what was given and when. Appreciated stock, real estate and other assets all carry different tax treatments when transferred during your lifetime versus at death. In some cases, your heirs would pay less in taxes if they inherited the asset and received a stepped-up cost basis rather than receiving it as a gift with your original basis attached. The right answer depends on the specific asset, your tax situation and your heir’s tax situation, and it can change over time.

This is where the Form 709 filing connects back to your broader estate plan. Every gift you make shifts the balance between what you transfer now and what your estate transfers later, and each path has different tax consequences. A financial advisor or estate planning attorney can help you see how a gift you are considering today fits into the larger picture, including how it affects your remaining exemption, whether it creates a tax issue for the recipient, and whether the same goal could be accomplished more efficiently another way. The form itself is just paperwork. The planning behind it is what determines whether the gift actually accomplishes what you intended.

Bottom Line

Unless you made a taxable gift valued at more than $19,000 to an individual or entity in 2026 (or 2025) you don’t need to fill out Form 709. If you did, you may just need to report the gift. You won’t owe an out-of-pocket tax until you’ve given more than your lifetime gift and estate tax exemption. That currently stands at $15 million for tax year 2026 (and $13.99 million for tax year 2025).

Additional Tax Filing Tips

- Some financial advisors can help you optimize your tax strategy for your financial goals. Finding a financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with vetted financial advisors who serve your area, and you can have a free introductory call with your advisor matches to decide which one you feel is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

- If you’re investing in a 529 college savings plan, you have some special gift tax exemptions. We cover these in our study on how to give money to students and avoid gift tax.

- If you don’t feel like filing taxes by hand, you can always use tax software to get it done and avoid mistakes.

Photo credit: ©iStock.com/Andrei Barmashov, ©iStock.com/Andrii Yalanskyi, ©iStock.com/LIgorko