If you don’t have a lot to spend on a down payment for a home, you may be a good match for an FHA loan. The Federal Housing Administration (FHA) backs loans to certain higher-risk applicants as a way to get more Americans onto the property ladder. Sound good?

We know what you’re thinking: “What does it mean when you say that FHA “backs” these loans?” Well, the FHA doesn’t technically act as the lender for your home loan. Instead, they insure the loan. A conventional lender like a bank acts as the loan servicer—i.e. the person who receives your monthly payment. So, you’ll still be dealing with conventional lenders, but you’ll be making a different kind of loan application—an FHA loan application, to be specific.

To be a candidate for one of these low-down payment mortgages, you’ll need to meet a few criteria. They don’t go around giving out FHA loans like candy. So how do you know if you meet the requirements? Here is a rundown of FHA qualifications.

Is the mortgage loan amount you’re seeking at or under the FHA maximum for your area?

FHA sets a maximum loan amount that varies from county to county, based on the price of local housing. These are generally between $275,000 and $650,000, although in some places the limit is even higher.

What’s your debt-to-income ratio?

First, add up all your regular monthly debt obligations—things like credit card bills, student loan payments and housing payments. When you make these calculations, don’t use your current housing payments—use what your monthly payment would be on your new house. Our mortgage calculator can help you figure out what this would be. Then, divide the number that represents your total monthly obligations by your gross monthly income. What’s your gross income? It’s all the money you make (from dividends and income) before taxes. The number you get when you divide your monthly debt by your gross monthly income? That’s your debt-to-income ratio. If it’s too high, you won’t qualify for an FHA loan. How high is too high? The numbers aren’t set in stone, but 43% is generally the absolute maximum, and it’s safer to shoot for 41%.

The debt-to-income ratio for just your housing expenses in the new home should be no more than 31%. In other words, your gross monthly income multiplied by 0.31 equals the monthly mortgage payment you can afford, according to FHA guidelines. If your ratio is at or under 29%, you’ll have an easier time getting a loan. If your ratio is above 31%, you may be able to get your lender to bend the rules, provided the rest of your application shows that you could handle the mortgage payments. Often, when you’re reviewing lenders’ requirements you’ll see debt-to-income ratio requirements expressed in pairs, with the first number showing the ratio for just your housing costs, and the second number showing the ratio for all your monthly debts (31/43, in our example).

How’s your credit?

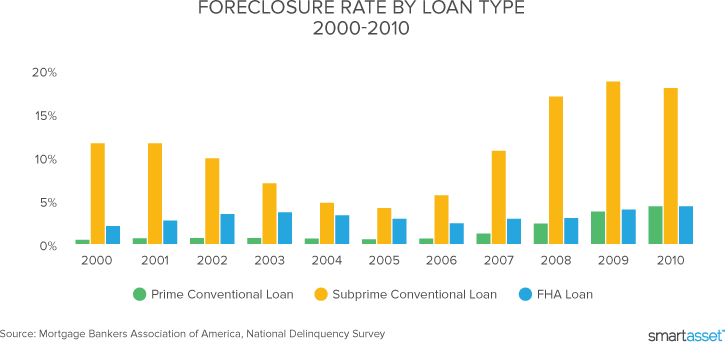

The state of your credit will be an important factor in determining your eligibility for an FHA loan. If you’ve been through foreclosure in the last three years, or bankruptcy in the last two, you will not meet FHA qualifications and are not a candidate for an FHA loan. To qualify for the 3.5% down payment, your credit score will need to be at least 580. With a lower score, you’ll need to put 10% or more down, and you may have trouble finding a lender who will work with you. As a rule, the better your credit, the more easily you will qualify for a home loan—FHA or otherwise.

Can you put at least 3.5% down?

The big advantage of an FHA loan is that you can get away with putting as little as 3.5% down, assuming your credit score is up to snuff. (Compare this to the 20% down payment required for most conventional loans.) Another bonus of an FHA loan? Up to 100% of your FHA down payment can come from a gift. If you can’t scrape together that 3.5%, though, you’ll have to wait and save up more down payment funds before getting an FHA loan.

How’s your employment history?

Have you had two years or more of steady employment? Been with the same employer that whole time? Lenders like to see that.

Will the home be your primary residence?

FHA loans generally aren’t available for vacation houses, ski chalets, hunting lodges, beach shacks, etc. They’re designed to help people finance homes that they will live in year-round.

Do you have all the relevant paperwork?

What kinds of things will you need to document? Your Social Security number, income, current address, employment history, bank balances, federal tax payments, any open loans and the approximate value of your current property. And that’s a minimal list. You’ll want to talk to a loan officer about the paperwork you’ll have to submit with your application. Then, start digging it all out and make copies. If you’re a veteran, you’ll need to submit extra paperwork related to your service record.

Keep in mind that individual lenders’ requirements may be more stringent than the FHA qualifications. When banks decide to offer FHA loans, they’re allowed to impose their own standards beyond those set out by the government. That’s why it pays to shop around for a lender before committing to a mortgage.

One last thing.

Just because you meet the FHA qualifications doesn’t mean it’s the best type of loan for you. If you put less than 10% down for an FHA loan, you’ll have to pay mortgage insurance premiums. Your FHA loan might also carry higher interest rates to make up for the low down payment. When you add those two factors together, you could be looking at a loan that’s costlier than a conventional loan would be. If your savings for a down payment don’t reach the 20% mark usually needed for a conventional loan, look into down payment assistance programs or family gifts. Getting some down payment assistance for a conventional loan might be cheaper in the long run than a low-down payment FHA loan. Alternatively, you could wait on the home purchase and build up your savings and investments. It’s worth considering all the options before making this large of a decision, and purchase.