Written by

Written by

As people age, their spending and saving patterns change. Major life events like buying a home, getting married or having kids may impact not only the rate at which people save, but also how they allocate the money that they do spend. Generational cohorts have also demonstrated differences in their financial priorities. For instance, a report from the Urban Institute found that in 2018, millennial homeownership rates were approximately eight percentage points lower than the homeownership rates of Generation Xers and baby boomers when they were the same age (21 to 37 years old).

In this study, we looked at how different generations spend money. Using data from the Bureau of Labor Statistics’ 2018 Consumer Expenditure report, we considered the three largest living generations in the United States – millennials (born 1981-1996), Generation X (born 1965-1980) and baby boomers (born 1946-1964) – and their spending according to 11 major categories. We grouped spending by needs and wants, defining housing, utilities & housekeeping, food, healthcare and transportation as needs and apparel & personal care products, entertainment, reading & education and alcohol & tobacco as wants. We additionally considered other spending on personal insurance and pensions along with miscellaneous expenses. Below, we discuss similarities and differences in 2018 spending across generations for those 11 major categories.

Key Findings

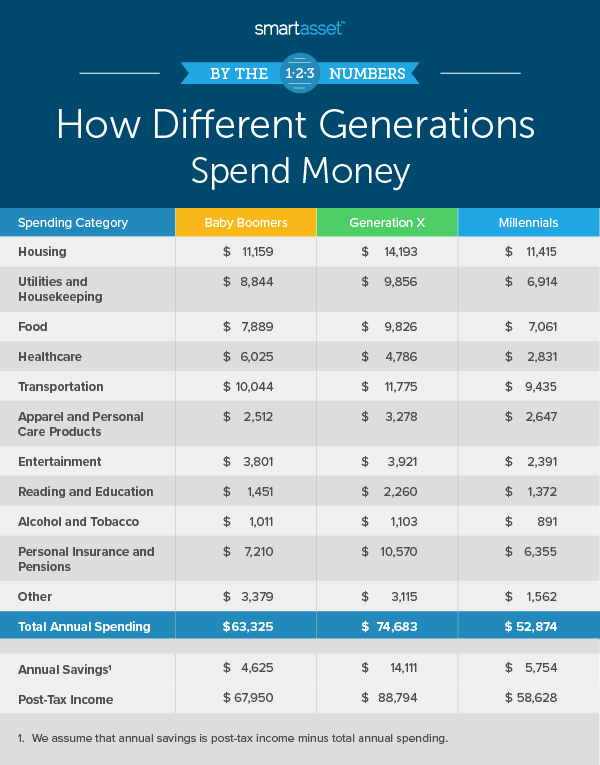

- Gen Xers have the highest post-tax incomes and spend the most. Millennials, Gen Xers and baby boomers had average post-tax incomes of $58,628, $88,794 and $67,950, respectively, in 2018. Of their post-tax income, millennials spent an average of $52,874 a year, while Gen Xers spent $74,683 and baby boomers spent $63,325 a year. That means Gen Xers outspend millennials and baby boomers by 41% and 18% respectively.

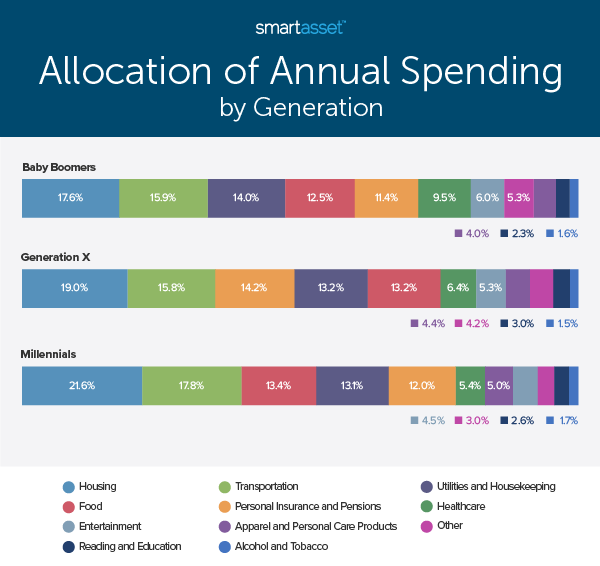

- Housing and healthcare spending vary the most by generation as a percentage of overall spending. Housing spending as a percentage of overall spending decreases as we look at older groups, with millennials allocating the highest percentage to rent and housing costs and baby boomers the lowest. By contrast, healthcare spending increases with each older generation. On average, healthcare spending makes up 9.5% of total spending for baby boomers compared to only 5.4% for millennials.

- Savings rates are below suggested levels for all three generations. Assuming people from each generation save all of the post-tax income they don’t spend in the defined categories, We found that millennials and baby boomers both save less than 10% of their post-tax income, while Generation Xers save about 16%. Those are all below the recommended savings rate of 20%, according according to a 50/30/20 budget plan.

Spending on Needs

Housing

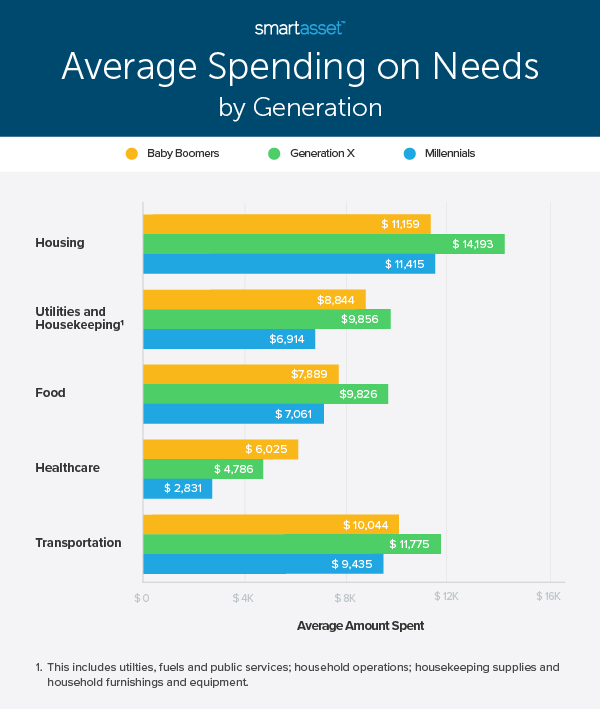

Millennials are less likely to be homeowners than Gen Xers and baby boomers. Census Bureau data shows that the under-35 homeownership rate was 33.7% in 2018 compared to the national average of almost 67%. Percentage-wise, millennials dedicate more of their annual spending to housing than any other generation does. Housing makes up almost 22% of annual expenditures for millennials relative to about 19% for Gen Xers and 17.6% for baby boomers. In gross terms, millennials and baby boomers both spend slightly more than $11,000 annually on housing, while Generation Xers spend about $14,200.

Utilities & Housekeeping

Utilities & housekeeping spending includes the following: utilities, fuels and public services; household operations; housekeeping supplies and household furnishings and equipment. Baby boomers allocate the greatest percentage of total spending to utilities and housekeeping, 14%. Though millennials only spend about half of their housing costs on utilities and housekeeping, baby boomers’ utilities and housekeeping spending is about 80% of their housing costs. Specifically, baby boomers spend an average of $8,844 on utilities and housekeeping relative to the $11,159 they spend on housing in total.

Food

As a percentage of annual expenditures, spending on food generally increases as we look at the spending habits of successively younger generations. Of the three generations for which we considered data, millennials dedicate the most of their annual spending towards food, at 13.4%, while baby boomers allocate the least, at 12.5%. Though Gen Xers fall between millennials and baby boomers when comparing food spending to overall spending, they spend the most in gross terms, an average of almost $10,000 per year.

Though we categorized food as a need, eating out in particular may be considered a want. The BLS Consumer Expenditure Survey distinguishes between spending on food at home and food away from home. Food away from home includes all meals including tips at fast food restaurants, cafeterias and full-service restaurants along with take-out and delivery. Perhaps expectedly and potentially driving up higher food spending percentages, millennials tend to spend more on eating out than Gen Xers and baby boomers, according to the data. Almost half of food spending for millennials goes towards food away from home, 47.3%, while baby boomers allocate only 41.7% of their total food spending to eating out.

Healthcare

As people age, the incidence of health conditions tends to rise. Unsurprisingly, healthcare spending, which includes health insurance, medical services, drugs and medical supplies, also increases as we look at data for older age groups. Across generations, from millennials to baby boomers, healthcare spending grows in both gross terms and as a percentage of annual spending. Millennials and Gen Xers spend averages of $2,831 and $4,786, respectively, on healthcare, which map to 5.4% and 6.4% of their total spending. Baby boomers, not all of whom were yet eligible for Medicare in 2018, spent the most – $6,025, or about 9.5% as a percentage of their total spending. Healthcare has the widest range of spending by generation, 4.1%, surpassing housing which has a range of 4.0%.

Transportation

Transportation expenses include vehicle purchases, vehicle insurance, gas and oil and public transportation fares. Transportation spending varies significantly less across generations than healthcare spending. In gross terms, average annual transportation spending for each of the three generations is about $10,000 – more specifically, at $9,435 for millennials, at $11,775 for Generation Xers and at $10,044 for baby boomers. Though as a percentage of annual spending, transportation spending decreases with older age groups – from 17.8% for millennials to 15.9% for baby boomers – the range across generations is much smaller here, at less than 2%, than the range of healthcare spending, which spans more than 4%.

Spending on Wants

Apparel & Personal Care

In the category of wants, millennials allocate a higher percentage of their total spending on apparel & personal care than other generations do. BLS data shows that millennials allocate about 5.0% of their spending to clothes, personal care products and personal care services relative to 4.4% by Gen Xers and 4.0% by baby boomers. In gross terms, millennials spent an average of about $2,600 on apparel & personal care in 2018.

Entertainment

Though millennials have gained a reputation for their spending on experiences, average millennial spending on entertainment is about $1,500 lower than that of each of the other two generations we examined. In 2018, millennials spent an average of $2,391 on entertainment, while Gen Xers and baby boomers spent an average of $3,921 and $3,801, respectively. As a percentage of overall spending, millennials still lag behind Generation X and baby boomers. About 4.5% of annual millennial spending is dedicated to entertainment relative to 5.3% of Gen X spending and 6.0% of baby boomer spending.

BLS categorizes entertainment spending according to five subcategories – fees and admissions; television, radio and sound equipment; pets; toys, hobbies and playground equipment; and other entertainment supplies, equipment and services. Across all ages, the majority of entertainment spending goes to the first three – fees and admissions; television, radio and sound equipment and pets. Specifically, about 80% of millennial entertainment spending, 80.7% of Generation X entertainment spending and 68.4% of baby boomer entertainment spending goes to those three subcategories.

Reading and Education

Though spending may be significantly higher for some Americans given the rising costs of higher education in the U.S., the average American spent between $1,300 and $2,400 on reading and education in 2018. As a percentage of total spending, millennials, Gen Xers and baby boomers allocated between 2% and 3% of their annual spending to reading and education. Gen Xers spent the most in gross terms, $2,260, and as a percentage of spending, 3.0%.

Alcohol & Tobacco

In gross terms, millennials spend about $200 less annually on alcohol, tobacco products and smoking supplies than Gen Xers do and about $100 less than baby boomers do. However, as a percentage of spending, Gen Xers allocate the least, about 1.5%, compared to 1.7% by millennials and 1.6% by baby boomers. In fact, alcohol and tobacco spending is the only category of the 11 we looked at for which Gen Xers allocate the least of their spending of the three generations.

Tobacco products and smoking supplies include cigarettes, e-cigarettes, cigars and smoking accessories. The breakdown in spending between alcohol and tobacco is also similar across generations; spending on alcoholic beverages is about 1.6 times the spending on tobacco products and smoking supplies. Millennials spent an average of $560 on alcohol and $331 on tobacco products and smoking supplies in 2018. By comparison, Gen Xers and baby boomers spent respective averages of $693 and $617 on alcoholic beverages and $410 and $394 on tobacco products and smoking supplies.

Other Spending

Personal Insurance and Pensions

Personal insurance and pensions spending include post-tax income spent on life, endowment, annuities and other personal insurance and retirement, pensions and Social Security. The BLS found that over the past year personal insurance and pensions spending increased the most of any major category, rising by 7.8% for all consumer units, from $6,771 in 2017 to $7,296 in 2018. Gen Xers had the highest average spending on personal insurance and pensions in 2018, roughly $10,500.

Cash Contributions and Miscellaneous

The remaining spending for each generation falls under the two BLS categories of cash contributions – cash contributed to persons or organizations outside of the consumer unit – and miscellaneous – which includes several subcategories such as bank service charges and credit card memberships. Baby Boomers have both the largest gross amount, $3,379, as well as percentage of their spending in this category of the three generations, at 5.3%.

Savings

We estimated the average annual savings for each generation by subtracting total annual spending in the 11 defined categories from post-tax income. In 2018, baby boomers saved the least in gross terms of all three generations, $4,625, and Gen Xers saved the most, $14,111. Baby boomers had the lowest savings rate of about 6.8% while Gen Xers had the highest, 15.9%. Millennials fell in the middle with a savings rate of 9.8%.

It is important to note that spending on pensions and Social Security, a subcategory of personal insurance and pensions, may also be counted as savings. Including pensions and Social Security spending along with the difference between annual spending and post-tax income, millennials, Gen Xers and baby boomers have savings rates of 20.3%, 27.2% and 16.5%, respectively.

Data and Methodology

Data for this report comes from the Bureau of Labor Statistics’ 2018 Consumer Expenditures Survey. All reported figures are averages per consumer unit. Consumer units include families, single persons living alone, single persons sharing a household with others while also remaining financially independent or two of more persons living together who share major expenses. The BLS measures the variability of average expenditures by calculating a coefficient of variation, which is the standard error divided by the mean expenditure and is expressed as a percentage. Per BLS recommendations, we did not rely on estimated averages with a coefficient of variation greater than 25.

Tips for Budgeting and Saving

- Make a plan, no matter your generation. The Consumer Expenditure Survey highlights how many Americans are not saving the recommended 20% of their post-tax income. One of the best ways to get your finances under control is by making a plan. Though generational spending patterns may vary, personal finance is, after all, personal. Take a look at our at our free budget calculator to map out your monthly and yearly expenses. Also take a look at our cost of living calculator to see how your city compares to others. The cost of living in a city can significantly affect your finances and ability to save.

- Invest early. By planning and saving early you can take advantage of compound interest. Take a look at our investment calculator to see how your investment can grow over time. This will prove a strategic way to grow your money as your spending and savings priorities change.

- Consider a financial advisor. Whether you’re a millennial starting your professional life, a mid-career Gen Xer or a baby boomer nearing retirement, a financial advisor can help you make smarter financial decisions to be in better control of your money. Finding the right financial advisor that fits your needs doesn’t have to be hard. SmartAsset’s free tool matches you with financial advisors in your area in 5 minutes. If you’re ready to be matched with local advisors that will help you achieve your financial goals, get started now.

Questions about our study? Contact us at press@smartasset.com

Photo credit: ©iStock.com/Hispanolistic