Single-family home, co-op, condo, townhome. Feeling overwhelmed by housing choices? We’re here for you. Step away from the real estate listings and check out our guide to the types of homes that are out there.

The Choices

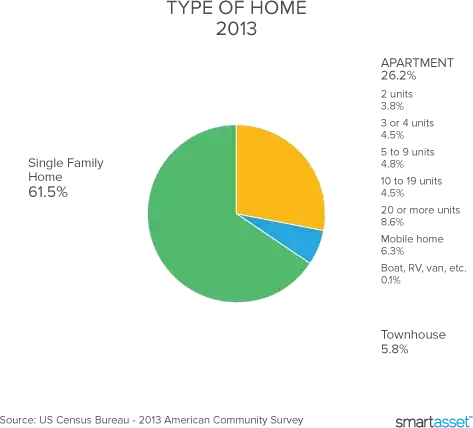

A single-family home is just what it sounds like. It’s a separate home meant for only one family. Specifically, it means the house isn’t attached to any others and has (at least some) open space on all four sides. Certain neighborhoods may have homeowners associations (HOA) but in most instances, the owner is responsible for upkeep costs of the home and the yard.

A townhome is similar to a single family home but generally you share a common wall with a neighbor. The property is owned from ground to ceiling so a townhome is often comprised of several floors – more narrow and vertical than sprawling. Townhomes may or may not include attached garages. While you may have some open space to the front or the back, it is sometimes maintained by a homeowners association. There also may be shared common areas like pools, parks or playgrounds. You, of course, pay a fee to the association to cover the upkeep.

A condo, or condominium, is a group of homes where the homeowner owns the air between, but not the actual, walls, ceiling or floors of the unit. So this means that usually the homeowners association will be in charge of things like cleaning the windows, repairing pipes and maintaining common areas like fitness rooms. Condo owners share ownership of those common areas. This type of home usually requires a monthly common charge for building upkeep. It can look like a tall building or not – like a duplex, fourplex or single-family home subdivided into multiple units.

Think it’s weird that you won’t own the walls? How about not owning the unit at all? A co-op is perhaps the most confusing of the options. That’s because co-ops aren’t considered real property. It may sound crazy but when you buy into a co-op, you actually become a shareholder in a corporation that owns the property. The property is usually a multi-family building and as shareholder, you are entitled to exclusive use of a unit in the property. They are popular in urban areas like New York City and require a monthly maintenance fee for upkeep. The board of the co-op has a lot of control over decisions relating to the building, including often approving potential new owners before allowing them to buy in. Because of this extra hurdle of need to find a buyer who makes an offer and also passes the board’s approval, re-sale of a condo can be a little more complicated.

To help you decide which of these types of homes is right for you, we’ll ask you a few questions.

How much space do you need?

Got a huge family? Three dogs? Lots of stuff? You may need to look for a big place. In most places around the country, this means a single-family home.

If you don’t need a lot of space, or you’re willing to trade some square footage for the perks of city living, consider a condo, co-op or townhome.

Are you DIY-obsessed?

With a co-op, condo or townhome in an association, you’ll be limited in the changes you can make to your place. You’ll need to get approval for any construction you do, which can be a hassle. If you’re dying to unleash your inner home improvement guru, a single-family home is your best bet (though there are some homeowners associations out there that can be strict as well). But if you’re an urbanite who doesn’t need the white picket fence experience, you’ll be looking at co-ops, condos and townhomes.

Can you handle co-op board drama?

Do you have a pet? Do you stay up late? Do you have kids? Do you make any noise ever? These are some of the questions you’ll likely face when you interview to join a co-op building. The approval process for these buildings is notoriously tough. So tough, in fact, that it’s not unheard of for sellers to sue their building’s co-op board for rejecting too many applicants and holding up the sale of a unit that’s on the market.

Even people with plenty of money get rejected. When a co-op board rejects your application they don’t have to tell you why, and unless they’re careless enough to give you a reason that’s outright discriminatory, you won’t have legal recourse.

Part of the reason these boards are such sticklers for finding the right fit is that co-ops are, well, co-operative. As a reminder - when you buy into a co-op building, you don’t actually buy your unit. Instead, you buy shares in the co-op corporation, and the shares then entitle you to a lease on the unit you’ll call home. All co-op residents split the cost of taxes on the building, utilities, staff salaries, insurance, upkeep and mortgage payments on the building. As you can imagine, these costs can add up, and if one member can’t or won’t pay, the others are in a bind. In a co-op, residents sink or swim together.

So you made it through the co-op approval process and you’re forking over the maintenance charges? Don’t think you’re set for life. If you buy into a co-op building, stay friendly with the board and be nice to your neighbors. Co-op boards can vote to evict residents, canceling shareholders’ leases.

Why would anyone put up with this? Some of urban America’s most historic, beautiful, and—let’s face it—prestigious buildings are co-ops.

Do you love city living but fear co-ops?

If this is you, consider the condo. When you buy a condo, you’re actually buying your living space, not buying shares and leasing your place as you would in a co-op building. Condos are often newer buildings that can come with perks like gyms or recreation rooms. The more of these perks you go for, though, the higher your association fees will be.

To fee or not to fee?

Homes need maintenance. Pipes burst, toilets break, laundry machines need to be replaced. To deal with these expenses, condos have common charges, while co-ops have maintenance charges. Often, utilities are included in these charges. A good building will tell you up-front what these charges are likely to be, but you’ll still need to be prepared for bearing your share of unexpected costs like a broken elevator or damage from a weather event.

Remember that if you own your home outright, you will still have to pay some money to maintain it—but you’ll be able to do this on your own schedule and to your own taste. You also won’t be paying for things like a gym you never use, or a lobby redesign you can’t stand.

If you like the idea of living in a neighborhood with some density but don’t want to pay the fees involved with condos or co-ops, consider the townhome. A townhome, also known as a townhouse or rowhouse, is a narrow dwelling that shares at least one wall (but no floors or ceilings) with an adjacent building. In other words, you won’t have upstairs or downstairs neighbors to worry about, but you will share what’s called a “party wall” with your next-door neighbor. In a townhome, you usually don’t pay association fees for upkeep of the exterior. You can even mow your own lawn if that’s your thing.

Although you’re responsible for the maintenance of your own townhome, you will have to deal with the homeowners association that handles common areas like courtyards or parks. Like co-op boards, HOAs can be magnets for petty squabbles and in-fighting. Want to paint your house off-white? You’ll need to run it by the homeowners association to make sure it’s the right shade of off-white. HOAs also charge fees for the upkeep of any common areas. These are generally lower than they would be in a co-op or condo building that has a full-time staff and a mortgage, though.

If you want the freedom to replace your lawn with wild grasses and sculptures made from recycled wine bottles, or you’re looking for a way to display your carefully-curated garden gnome collection, steer clear of a townhome or any development with an association. That’s because they come with Covenants, Conditions, and Restrictions (CC&R’s) that can cramp your style. Choose a single-family home instead and you can make your own rules. On the other hand, if you’re the person who gets annoyed by other people’s garden gnomes, maybe association living is perfect for you.

What’s your risk tolerance?

When you own a single-family home, the only person whose financial solvency you really have to worry about is your own. Of course, if the other houses on your block fall into disrepair or default you won’t be able to get as much for your house when you want to sell. But with a single-family home you won’t owe fees that could increase with every neighbor who defaults or vacates a unit.

Eligible owners of single-family homes, townhomes and condos can also get cash relatively quickly through second mortgages, cash-out refinancing and home equity loans. Those in co-op buildings will have to get board approval to refinance, and will also need to accept the risk that it will take a long time to sell should they decide to move. Remember those finicky co-op boards?

Here’s hoping we’ve helped you get clarity on the different types of homes out there! Now that you have chosen from the different types of homes the one that is best for you, hop on our tool to find out how much house you can afford.