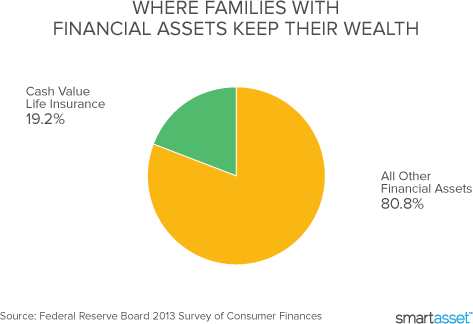

Life insurance, whether term or cash value, is a way to protect your dependents in the event you’re no longer able to contribute to their financial well-being. What’s the difference between the two forms of life insurance? And how does cash value life insurance work?

Cash value life insurance, also known as permanent life insurance, does two things. It pays out when the policyholder dies, and it accumulates value while the policyholder is alive. You can use cash value life insurance as a form of tax-sheltered investment and earn modest returns on your premium payments. You can even use the earnings from your policy to pay the monthly premiums or withdraw cash for income. Whole life, variable life and universal life are all forms of cash value life insurance.

The alternative to cash value life insurance is term life insurance. With term you insure yourself for a specific number of years, say until your kids graduate college or the mortgage is paid off. If you die within the term, the insurance company pays up. If you outlive the term (and we certainly hope you do) the policy ends and you don’t get any money out of it.

Many people don’t like the fact that, with term life insurance, you pay premiums each month and don’t see any of that money back at the end of the term. For these people a cash value insurance policy may sound like a more appealing option. Read on to find out some cash value life insurance pros and cons.

The pros of cash value life insurance

- Access to your premiums: With term life insurance, the money you pay to the insurance company in premiums is lost forever (except with a return of premium policy). The insurance company keeps it and you have no further claim on it. But with cash value life insurance, part of the money you pay in premiums contributes to your cash value account and forms your "basis" in the policy. You can borrow from your cash value account tax-free later down the line. Depending on the specifics of your policy there may be fees. Wondering how to calculate the cash surrender value of your life insurance? Its cash value is the stated face value of the policy. The amount you can access without paying taxes is the face value minus your basis and any withdrawals you’ve already made.

- Tax-free earnings: The cash value of your life insurance policy and the earnings that it makes grow tax-free. When you withdraw money, as long as you only withdraw up to the amount you’ve paid in premiums, you won’t owe any taxes on that money. If you withdraw more than that, though, you are actually taking out some of the interest your money has earned. In this case you’ll have to pay taxes on the difference between what you paid in and what you’re taking out. In other words, a chunk of your policy’s cash surrender value is taxable.

- Money in your pocket: If you want to access the cash value of your policy, you are free to do so. You can withdraw the money to help pay for retirement or to pay your life insurance premiums. You can also take out a loan against the cash value of the policy, though if you die without paying the loan back, your beneficiary’s payout will be lowered by the amount of the loan. If you borrow against the full value of your life insurance policy and then get hit by a bus (sorry) before you pay back the loan, your family won’t get anything.

- You’re insured regardless of how your health evolves: With term life insurance, if your health declines over the coverage term and you need to re-up your coverage (buy another term), you may have a hard time doing so or you may need to pay higher premiums. But with a cash value life insurance policy, you are covered even if changes in your health, lifestyle or occupation make you more of a risk to the insurance company. You will generally pay a flat — but high — rate for premiums for your whole life.

The cons of cash value life insurance

- Earnings won’t go to beneficiaries: When you die, your beneficiary will get the face value of your policy (the amount your life was “worth”) and won’t see any of the earnings. The investment feature of cash value life insurance only works to your benefit if you tap the money while you’re alive. In other words, cash surrender value accounting differs depending on whether the original policyholder is the one accessing the money or whether the money passes to a beneficiary. Any cash value life insurance calculator worth its salt will take this difference into account.

- Low rate of return: Compared to stocks, the investment portion of cash value life insurance makes pretty paltry returns. Could you make more if you invested the money elsewhere? Likely yes — unless you are an extremely conservative investor.

- High fees and commissions: Cash value life insurance policies can come with high fees and agent commissions, both of which take a chunk out of your investment earnings. You may also get hit with a surrender charge if you decide to withdraw from the policy, even if you only withdraw up to the value of your basis.

- High premiums: Compared to term life insurance, cash value life insurance will saddle you with hefty monthly premiums.

- Loans carry interest: If you don’t want to pay the surrender charge for withdrawing money from your policy, you can access the funds by asking the life insurance company for a loan, with the policy value as collateral. The insurance company will charge you interest for the privilege, though.

Alternatives to cash value life insurance

- Build up savings in another vehicle: Cash value life insurance isn’t your only option for building up savings. If risk isn’t your thing, you may want to consider bonds and CDs.

- Invest your money: That’s right, we’re talking about the stock market. If you’re tempted by a cash value life insurance policy you’re probably a conservative investor, which could mean you’re nervous about investing in stocks (also known as “equity exposure”). But if you want to see big returns on your money and you can afford to weather some ups and downs in the market, investing in an index fund with a low expense ratio just might be your best bet.

A note to the super-rich…

Hey there. If you have a very high net worth (you know who you are) you’re probably concerned about how your family will cover all the estate taxes that the government will claim when you die. A life insurance policy can be a good way to earmark money for paying off estate taxes. Why? Because the policy payout can pass straight to your spouse when you die, without going through probate court and without being subject to estate taxes. This only works if you name your spouse as the beneficiary rather than naming your estate as the beneficiary. Then, he or she can use the life insurance money to pay the Tax Man.