Written by

Written by

The recession, inflation and COVID-19 have made a bad situation worse. Financial dependency now has aging parents living with their adult children and their adult children footing the bill for their parent’s ill-planned retirement. All while also trying to raise kids, buy a house, pay off student loans and save for their own retirement. The result? A continuous cycle of financial dependency based on generational enablement.

Below we’ll look at what is called the “sandwich generation,” how financial burdens from parents and children put strain on this cohort and how a financial advisor can help you break the cycle.

What Is the Sandwich Generation?

The sandwich generation is comprised of adults who are caring for kids of their own who are still under the age of 18 while providing care and/or financial support to their aging parents. This typically is in addition to their own financial responsibilities such as paying off debt (student loans, mortgage, etc.), saving for their kid’s college education and socking away money for their own retirement.

The result? A continuous cycle where the adult kids who cared for their parents, often become the burdensome aging parents who also need financial assistance during retirement from their kids.

The Stats Behind The Sandwich Generation

Here are some facts about the generation of adults who are “sandwiched” between providing care to their children and their aging parents (65+).

People are living longer: By 2060, life expectancy for the total population is projected to increase by about six years, from 79.7 in 2017 to 85.6 in 2060 (Census.gov 2020)

- The Outcome: There are more aging parents now than there used to be, and this number is likely to continue growing as technology and modern medicine prevail.

The sandwich infliction does not discriminate. Everyone, both men and women, are equally as likely to be a part of the sandwich generation. There are also no trends across racial or ethnic demographics that show one profile of person being more likely to join the sandwich generation cohort. (Pewresearch.org 2022).

- The Outcome: This is a problem that the entire population needs to be aware of because no one is exclusively safe from the effects of being in this group.

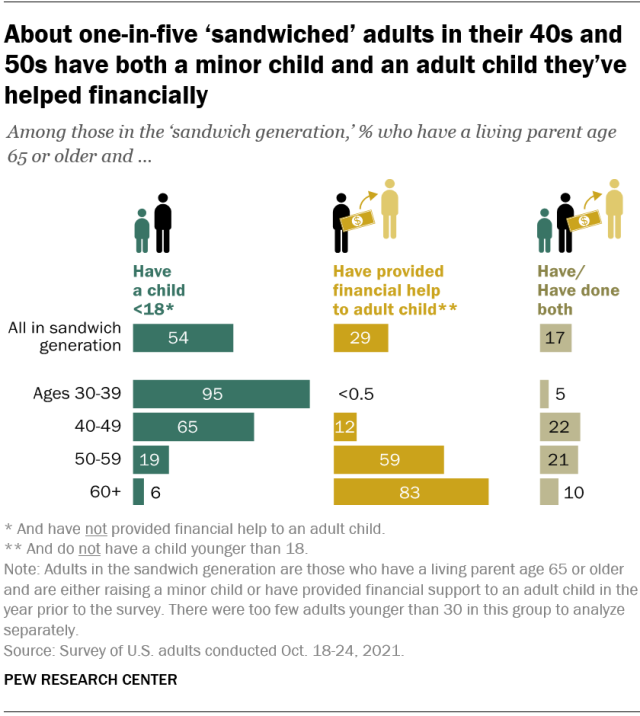

1 in 5 adults in their 40s and 50s help both a minor and an adult child simultaneously. About 17% of these adults offer financial assistance to their kids, at least one being a minor and another 18 and older. About 54% still support a child under 18, while 29% still support an adult child (18+). ( Survey of U.S. adults 2021).

{kind=link}

- The Outcome: In past years, the sandwich generation was typically one-sided in that you had an adult in his 40s assisting their aging parents 65+ while supporting kid(s) under 18. Today, with the cost of living, kids are relying on their parents to supplement their lifestyle for much longer. This is resulting in a longer overlap where adults in their 40s are financially providing for three generations of adults from one household income.

How to Plan Ahead

- Communicate: To plan for an elderly parent’s future, sandwich adults must gather information on their income, expenses, lifestyle, and financial status. This requires having discussions with the parent now.

- Analyze your financial situation: Organize account information, including retirement, bank, investment, credit card, insurance, trust and other accounts. Budget for long-term care costs by discussing all sources of income and essential/discretionary expenses, including federal/state benefits and tax consequences.

- Estimate expenses for future incapacity. Assisted living costs average $50K/year, while nursing home care can exceed $100K/year, possibly reaching $135K by 2028. Plan now to cover these costs.

What to Do When you Can’t Get Ahead

Planning ahead requires you to be proactive with your finances, which isn’t often a luxury afforded to many. If you’re past the point of no return and in the enablement cycle of the sandwich generation, there are some guiding principles to follow to keep you on track.

- Do not pause your retirement savings. The best thing you can do for yourself and your future generation is to stop the cycle from continuing. This means making sure you are self-sufficient in retirement and not burdening your adult kids with financial needs.

- Take advantage of tax credits. Those who offer care to dependents and make under $438,000 are eligible for the child and dependent care credits.

- Speak to a professional. A financial advisor might be able to help you ease the blow of financially supporting multiple family members simultaneously. You can likely find one that has experience with sandwich-generation adults and their most pressing concerns.

The Bottom Line

It’s never too early to start speaking with your parents about their retirement and what help they may be expecting from you as their adult child. By having the difficult conversations now, you may be saving yourself and future generations from financial hardship.

Tips for Investing

- Consider talking to a financial advisor about how to manage your financial plan if you’re taking care of parents and children. SmartAsset’s free tool can match you with up to three local financial advisors, and you can choose the one who is best for you. If you’re ready, get started now.

- A key part of financial planning in the sandwich generation involves Social Security and Medicare. Specifically, that means helping your parents decide when to take Social Security if they aren’t receiving benefits yet while also thinking about your own Social Security plans.

Photo credit: istockphoto.com/Monkeybusinessimages, skynesher,