Written by

Written by

Though they comprise a relatively small fraction of total homes, the number of million-dollar homes in the U.S. is growing. In 2016, about 2.3 million homes were worth $1 million or more. Meanwhile, in 2019, that figure was roughly 3.1 million. However, compared to the total 78.7 million owner-occupied homes, less than 4% of homes are worth $1 million or more. Million-dollar homes are highly concentrated in some states and cities more than others – and for homeowners who may potentially be seeking to upgrade, it could be worth it to seek the services of a financial advisor. In this study, SmartAsset investigated the cities with the most million-dollar homes.

We looked at the 150 largest U.S. cities to analyze the number of owner-occupied million-dollar homes compared to the number of owner-occupied homes. We additionally looked at the cities where the share of million-dollar homes is increasing the most by comparing 2016 and 2019 data. For details on our data sources and how we put the information together to create our findings, check out the Data and Methodology section below.

Key Findings

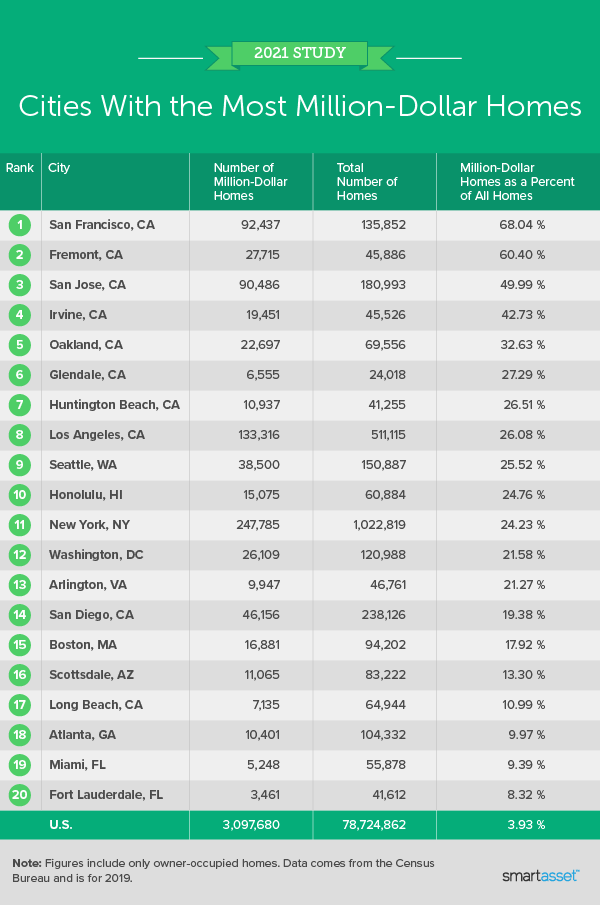

- In 13 cities, more than one in five homes are worth at least $1 million. When compared with the national share of million-dollar homes (3.93%), Census Bureau data shows that million-dollar homes are not necessarily an anomaly, comprising a much larger share (20%) in 13 cities. The first eight of these 13 cities are in California: San Francisco, Fremont, San Jose, Irvine, Oakland, Glendale, Huntington Beach and Los Angeles.

- Cities with the most million-dollar homes are concentrated on the coasts. From the top 20 cities with the most million-dollar homes, 17 are located on either the East or West Coast of the contiguous U.S. The three cities on neither of these coasts are Honolulu, Hawaii; Scottsdale, Arizona and Atlanta, Georgia.

Cities With the Most Million-Dollar Homes

San Francisco, California has the highest median home value across the 150 cities in our study and also ranks No. 1 for its percentage of million-dollar homes. Close to seven in 10 owner-occupied homes in area are worth upwards of $1 million. About one-third of million-dollar homes in San Francisco are fully paid off, a slightly lower percentage than the national rate, which shows that about 37% of million-dollar homes are paid off.

Across the Bay, Fremont, California follows closely behind San Francisco for its concentration of million-dollar homes and is the only other city where over one in two homes is worth more than that threshold. According to Census Bureau data, about 60% of homes there are worth $1 million or more. The median home value in Fremont is $1,086,700.

While the two largest U.S. cities – New York, New York and Los Angeles, California – rank No. 11 and No. 8, respectively, for their share of million-dollar homes, not all of the most populous cities make the list. The three other largest cities – Chicago, Illinois; Houston, Texas; and Phoenix, Arizona – do not rank in our top 20, shown below. The shares of million-dollar homes in Chicago and Houston are comparable to the national average, while only 2.33% of Phoenix homes are worth at least $1 million.

Cities Where the Share of Million-Dollar Homes Is Increasing

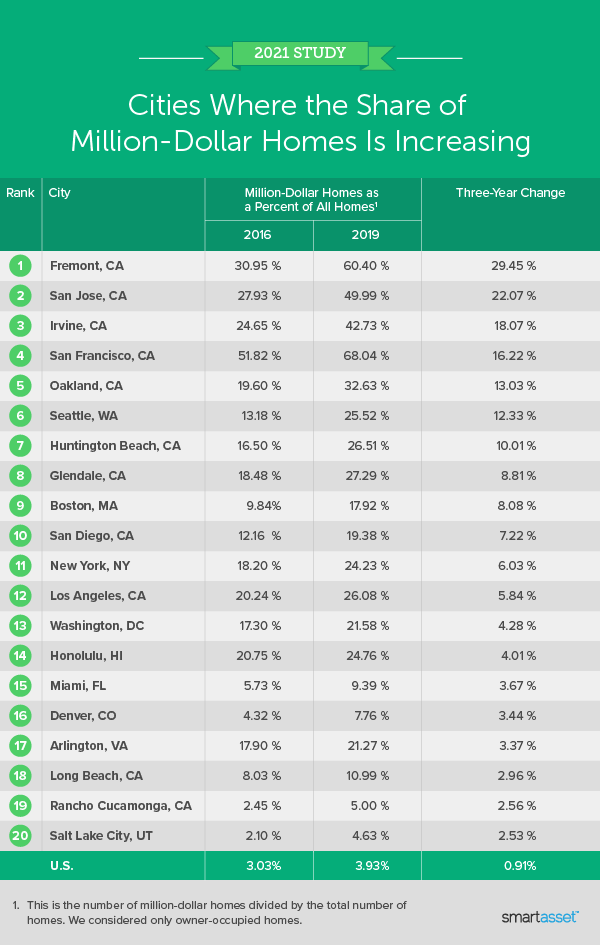

From 2016 to 2019, the share of million-dollar homes increased the most in two cities in California’s Bay Area: Fremont and San Jose. In 2016, less than 31% of homes in Fremont were valued at $1 million or more. However, by 2019, million-dollar homes made up more than 60% of homes in the area – roughly a 29 percentage point increase. The increase in San Jose was slightly lower, at about 22 percentage points.

In five other cities, the three-year percentage point change in the share of million-dollar homes was greater than 10. These include four California cities (Irvine, San Francisco, Oakland and Huntington Beach) and Seattle, Washington. The table below shows the 20 cities where the share of million-dollar homes increased most from 2016 to 2019.

Data and Methodology

Data for this report comes from the Census Bureau’s 2016 and 2019 1-year American Community Surveys. For both sections, we considered the 150 largest cities in the U.S. To find the cities with the most million-dollar homes, we divided the number of owner-occupied million-dollar homes by the number of owner-occupied homes. To find the cities where the share of million-dollar homes is increasing, we calculated the percentage point increase between the percentage of million-dollar homes in 2016 and 2019.

Tips for Understanding How Much to Spend on a Home

- Do the math. When deciding how much to spend on a home, be sure to calculate out your monthly mortgage payment along with any additional fees, taxes or insurance. If you want to work backwards, you can instead use our How Much House Can I Afford Calculator? It lets you enter your location, annual income and expected down payment to see what makes sense in terms of how much to spend on a home.

- Consider a financial advisor. Buying a home is a big decision and it may be a good idea to consult a financial advisor to better understand your financial situation and what kind of house you can afford. SmartAsset’s free tool matches you with financial advisors in five minutes. If you’re ready to be matched with advisors that may be able to help you achieve your financial goals, get started now.

Questions about our study? Contact us at press@smartasset.com.

Photo credit: ©iStock.com/KingWu