Written by

Written by

Estimates on the return on investment from having a financial advisor vary. In a 2019 whitepaper, Vanguard assessed an “Advisor’s Alpha,” or the value that a financial advisor adds to a client’s portfolio, to be about a 3% net return per year, depending on a client’s circumstances and investments. Separately, Morningstar researchers calculated how much better off clients are after engaging in optimal financial planning strategies. They found a 1.82% annual net difference between a typical baseline investment portfolio and an advisor-optimized portfolio.

However, the benefits of working with a financial advisor may be more easily defined qualitatively. Commonly cited benefits for clients include developing a holistic personal financial plan, having regular check-ins on progress toward financial goals and helping people make smarter financial decisions. To help contextualize the value of financial advice, we asked financial advisors about their value proposition, surveying about 160 advisors who are part of our SmartAdvisor platform that connects consumers with financial advisors.

Specifically, we explore the impetus for hiring a financial advisor. What are the investment habits and mistakes of prospective and new clients? Why are they seeking out a financial advisor? What do financial advisors see as the biggest benefit of working with a financial professional and what are the most common follow-up concerns of potential clients? For more information on our survey data, check out the Data and Methodology section below.

Key Findings

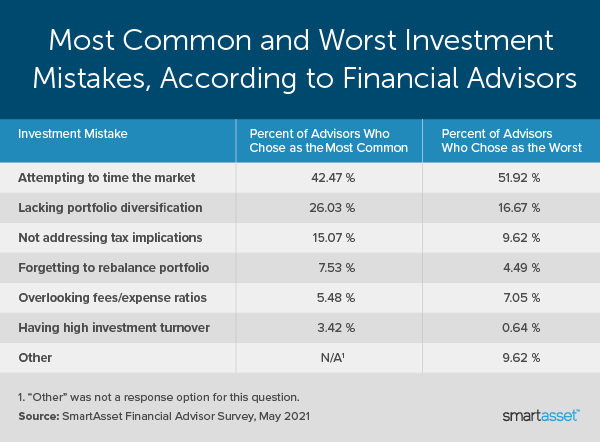

- Attempting to time the market is both the most common and worst investment mistake, according to advisors. About 42% of financial advisors say that attempting to time the market is the most common investment mistake they see among prospective and new clients. Even more financial advisors – close to 52% – say this is the worst investment mistake individuals make in general. Research agrees. A Merrill Lynch study found that model portfolios over a 30-year period could underperform by nearly half their value through market timing.

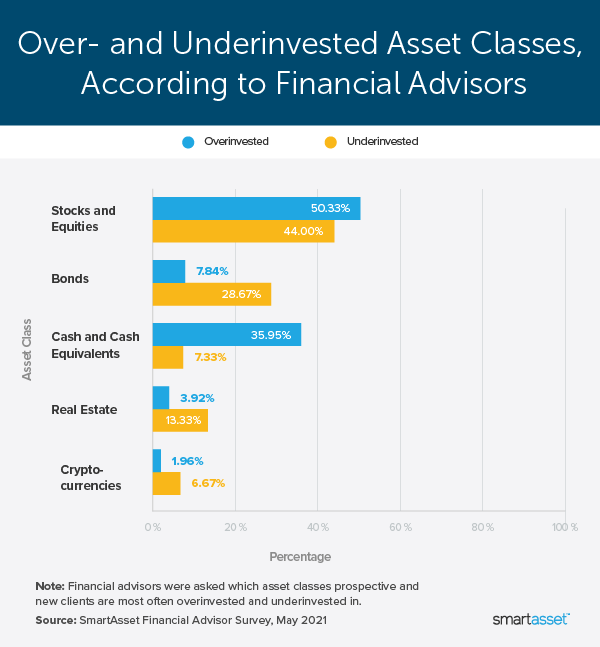

- Advisors are divided on whether clients are over- or underinvested in stocks and equities. Roughly half of advisors report that new and prospective clients are most commonly overinvested in stocks and equities. Interestingly, however, a high percentage of advisors (44%) also report that individuals are underinvested in this asset class.

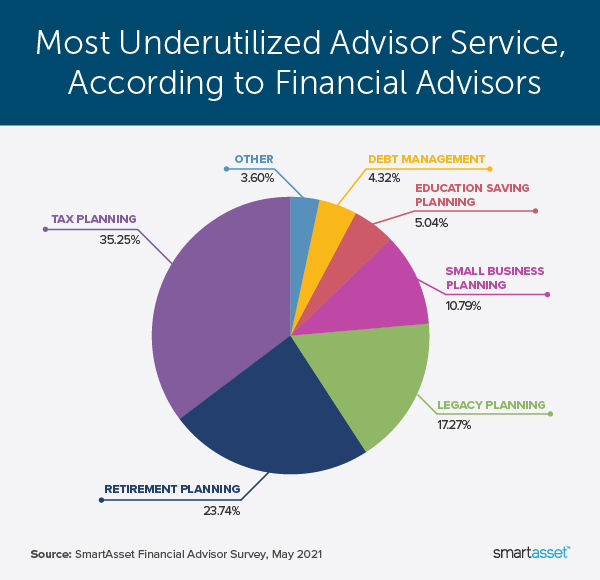

- Many advisors say their tax planning services are underutilized. Not all financial advisors provide tax planning advice to clients, but taxes can have a significant impact long-term on building wealth. More than 35% of surveyed advisors list tax planning as the most underutilized advisor service – ahead of both retirement and legacy planning.

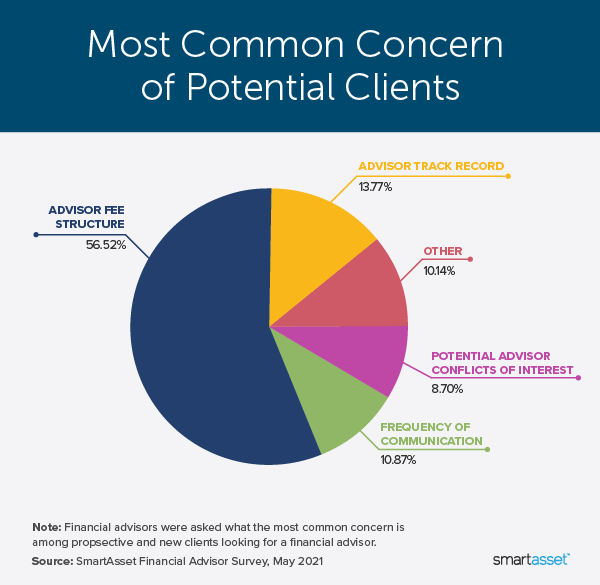

- Misconceptions about fees are common. Close to 57% of surveyed financial advisors cite advisor fee structure as the most common concern among prospective and new clients. When asked about common misconceptions, many advisors additionally say that consumers often believe financial advisors are “too expensive” or “cost too much.” If you are considering working with a financial advisor and want to get a better idea of the cost, our comprehensive guide here can help. Most financial advisor firms charge fees based on a percentage of assets under management (AUM). The average fee for these firms is about 1% of AUM, which amounts to $10,000 per year for a $1 million account.

Investment Habits and Mistakes

Prospective and new clients receive financial advice from a wide range of sources, according to financial advisors. The most popular source is free financial content online (from websites such as Investopedia or SmartAsset.com), and the next most popular source is a previous financial advisor. Regardless of where investors receive their financial advice, however, they tend to invest in similar ways. Almost three in four financial advisors (71.52%) say that prior to working with them, prospective and new clients were primarily using self-directed retirement accounts such as a 401(k) or IRA to invest their money. Meanwhile, less than 9% of advisors report that clients were primarily investing their money through self-directed, taxable brokerage accounts.

Among prospective and new clients who are investing their money through self-directed accounts, financial advisors list several common mistakes. The top ones include attempting to time the market, lacking portfolio diversification and not addressing tax implications. Along with being the most common, financial advisors also list these three mistakes as the most egregious. The table below shows the most common and worst investment mistakes according to financial advisors.

Because inadequate portfolio diversification is the second-most common investment mistake among prospective and new clients, we asked financial advisors the asset classes investors are overinvested and underinvested in. Beyond stocks and equities, advisors say that prospective and new clients are often overinvested in cash and underinvested in bonds.

Reasons for Seeking Out a Financial Advisor

Retirement planning is, by far, the most common reason investors look for a financial advisor. More than 72% of surveyed financial advisors list it as the top reason why most prospective and new clients search for a financial advisor. The second-most common reason, according to financial advisors, is improving investment returns, which nearly 30% of financial advisors listed as either the top or second-highest priority for potential clients.

Financial Advisor Services

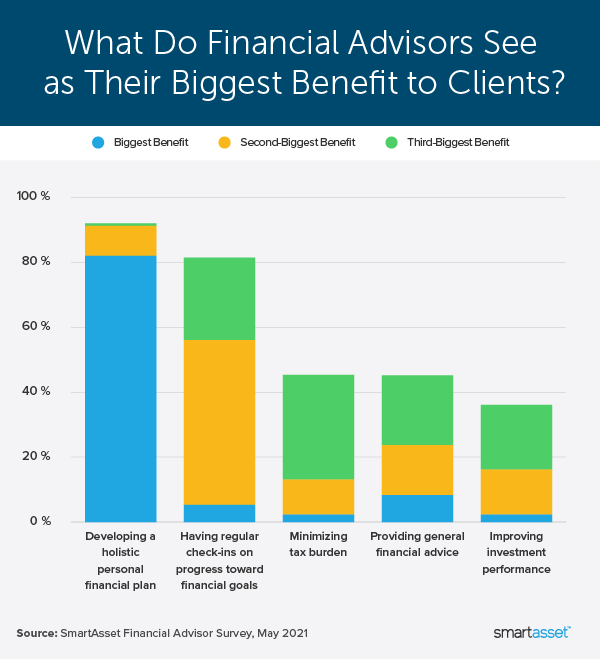

About 55% of financial advisors say that prospective and new clients have unrealistic return expectations. In fact, when considering their own services, financial advisors report that their value proposition is more than simply improving their clients’ investment returns. More than four in five financial advisors say that the biggest benefit advisors offer to their clients is helping them develop a holistic, personal financial plan. This benefit is followed closely by having regular check-ins on progress toward financial goals. Though about a third of advisors list improving investment returns as a top-three benefit for clients, less than 3% rank it as the No. 1 benefit.

Minimizing their clients’ tax burden is also not a No. 1 benefit according to most financial advisors, though a significant percentage of advisors rank it as a top-three benefit. Many advisors also say that it is one of the most underutilized client services, as previously noted. Retirement planning and legacy planning are the second- and third-most underutilized financial advisor services according to our survey. Roughly 24% of advisors say that retirement planning is the most underutilized service and about 17% responded that legacy planning is the most underutilized.

Common Potential Client Concerns

As previously noted, advisor fees are a top concern for prospective and new clients of financial advisors. Additionally, many potential clients are concerned about advisor track records and communication frequency. More than one in 10 advisors lists each of those two concerns as the most common among prospective and new clients. While it was not listed as an option in our survey, multiple advisors wrote that “trust” was a top concern among prospective clients. Prospective and new clients want to feel comfortable with the financial advisor they decide to work with and that their money is in good hands.

Data and Methodology

Survey data for this report was collected by SmartAsset between May 10, 2021 and May 26, 2021. A total of 159 financial advisors responded to our survey. Though the full survey was 13 questions, some advisors chose to skip certain questions. We used the largest sample possible when discussing results for any given question.

Tips for Finding Your Best Financial Match

- Individuals: Invest in expert advice. A financial advisor can help you make smart decisions to reach your investing and retirement goals. SmartAsset’s free financial advisor matching tool can connect you with up to three advisors who are fully vetted and free of disclosures. From there, you can speak with each one and decide how you want to move forward.

- Advisors: Pre-screen for prospects that meet your client profile. Consider using a service that can connect you directly with prospective clients. If you’re looking to grow your practice, SmartAdvisor connects advisors directly with local prospects. You pay only for investors that fit your client profile.

Questions about our study? Contact us at press@smartasset.com.

Photo credits: ©iStock.com/kate_sept2004