Written by

Written by

Individuals with higher levels of financial literacy tend to adhere to better financial practices – such as having an emergency fund and planning for retirement – and are also more likely to build wealth further by investing in the stock market. Many Americans, however, lack financial knowledge and do not follow financial best practices. Less than 50% of American adults have set aside three months’ worth of emergency funds, only 41% have tried to figure out retirement savings needs and just 32% have investments apart from retirement accounts.

In light of Financial Literacy Month this April, SmartAsset took a closer look at financial literacy in the U.S. In this study, we discuss the growing number of states with financial education standards along with how adults fare when asked a series of economics and personal finance quiz questions. Using data from the Financial Industry Regulatory Authority (FINRA) Foundation, the Council for Economic Education and Experian, we then identify the states where residents are most and least financially literate. For details on our data sources and how we put all the information together to create our findings, check out the Data and Methodology section below.

Key Findings

- A mismatch exists between perceived and tested financial literacy. The Financial Industry Regulatory Authority (FINRA) Foundation said in a recent national financial capability survey that roughly 71% of American adults believe they have a high level of financial literacy. However, when tested on personal finance topics, respondents struggle. On average, adults surveyed were able to answer only half of the literacy questions correctly.

- Midwestern states perform well while Southern states fall behind. More than half of the 10 most financially literate states are in the Midwest: North Dakota, Minnesota, Nebraska, South Dakota, Kansas and Wisconsin. All of them rank in the top 10 states for our financial knowledge & education index. At the other end of the study, Southern states rank in the bottom 10: West Virginia, Louisiana, Georgia, Texas, Tennessee and Delaware. All of these except Tennessee rank in the bottom 20 states on our financial knowledge & education index.

Financial Education and Literacy in the U.S.

The number of states requiring that personal finance be included in their standards has grown substantially over the past two decades. According to data from the Council for Economic Education, only 21 states included personal finances in their K-12 standards in 1998, relative to 45 states in 2020. Notably, only some states additionally require that these standards be implemented by individual districts within the state. In 1998, 14 states required that personal finance K-12 standards be implemented, compared to 37 states in 2020.

Though the prevalence of financial education in the U.S. is growing, many adults struggle when asked to respond to questions covering fundamental concepts of economics and personal finance. The FINRA Foundation’s National Financial Capability Study asks respondents a series of six quiz questions, shown below. Multiple choice answers are shown below the questions. Correct answers are listed at the end of the study in the Data and Methodology section.

- Mortgage Question: A 15-year mortgage typically requires higher monthly payments than a 30-year mortgage, but the total interest paid over the life of the loan will be less.

a) True

b) False - Interest Rate Question: Suppose you had $100 in a savings account and the interest rate was 2% per year. After 5 years, how much do you think you would have in the account if you left the money to grow?

a) More than $102

b) Exactly $102

c) Less than $102 - Inflation Question: Imagine that the interest rate on your savings account was 1% per year and inflation was 2% per year. After 1 year, how much would you be able to buy with the money in this account?

a) More than today

b) Exactly the same

c) Less than today - Risk Question: Buying a single company’s stock usually provides a safer return than a stock mutual fund.

a) True

b) False - Compound Interest in Debt Question: Suppose you owe $1,000 on a loan and the interest rate you are charged is 20% per year compounded annually. If you didn’t pay anything off, at this interest rate, how many years would it take for the amount you owe to double?

a) Less than two years

b) At least two years but less than five years

c) At least five years but less than 10 years

d) At least 10 years - Bond Price Question: If interest rates rise, what will typically happen to bond prices?

a) They will rise

b) They will fall

c) They will stay the same

d) There is no relationship between bond prices and the interest rate

On average, adults surveyed were able to answer only half (i.e. 3.0) of the above questions correctly. In fact, only 7% of adults were able to correctly answer all six questions. About 34% and 40% of surveyed adults were able to answer five and four questions, respectively. The compound interest in debt and bond price questions were the most difficult for respondents. Less than one in three respondents were able to correctly answer either question. Meanwhile, more than 70% of adults correctly answered both the mortgage and interest rate questions.

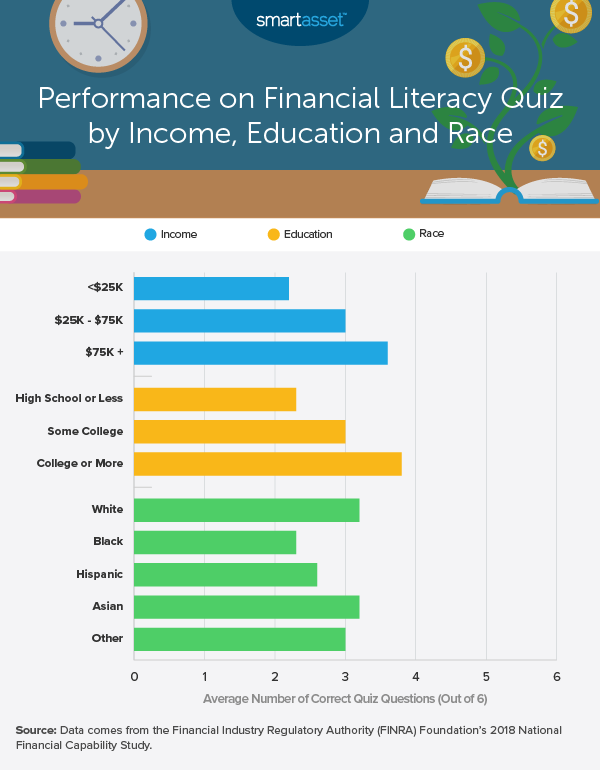

Notably, there are distinct differences in performance on the financial literacy quiz questions across different demographics according to education, income and race. The average number of correct quiz questions among individuals earning $75,000 or more and college graduates is 3.6 and 3.8, respectively. In contrast, individuals earning less than $25,000 and those with a high school education or less answered an average 2.2 and 2.3 questions correctly. The chart below breaks out survey respondents by race, showing the average number of correct answers for each group.

States Where Residents Are Most Financially Literate

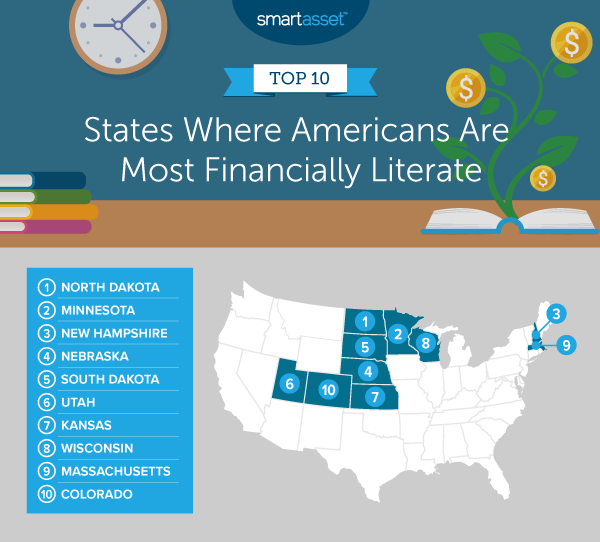

North Dakota ranks as the state where residents are most financially literate, taking the top spot on our financial knowledge & education index and the third spot on our financial practices index. According to the Council for Economic Education, the state of North Dakota requires that personal finance coursework be integrated into another course in the K-12 curriculum. In 2018, residents correctly answered about 55% of the National Financial Capability quiz questions discussed previously – almost five percentage points higher than the national average.

Minnesota and New Hampshire follow closely behind North Dakota. Minnesota is the top-ranking state on our financial practices index and ranks fifth on our financial knowledge and education index. Minnesota residents have the highest average credit score (739) of any state and the eighth-highest percentage of adults who report paying their credit card bill in full monthly (58.04%).

Six of the remaining seven states where residents are most financially literate are located in the Midwest and West. They include Nebraska, South Dakota, Kansas and Wisconsin in the Midwest, plus Utah and Colorado in the West. All of these states require that personal finance be included in K-12 standards and survey adults rank within the top 12 of the study on FINRA’s financial literacy six-question quiz.

States Where Residents Are Least Financially Literate

West Virginia ranks as the state where residents are least financially literate, with the lowest financial knowledge & education index and third-lowest financial practices index. West Virginia ranks in the bottom five states for three of the seven individual metrics we considered: percentage of adults that believe they have a high level of financial knowledge (67.37%), average percentage of personal finance quiz questions answered correctly (46.79%) and percentage of adults with a three-month emergency fund (42.53%).

Like in West Virginia, Nevada residents fall particularly far behind on our financial knowledge and education index. Though the state includes personal finance in its K-12 standards, only about two in three adults believe they have a high level of financial knowledge, the ninth-lowest of all 50 states and the District of Columbia. Additionally, the average percentage of correctly answered economics and personal finance quiz questions for Nevada is 49.14%, ranking within the bottom 15 of the study.

Across the eight other states where residents are least financially literate, three are not in the South: Indiana, Alaska and Pennsylvania. Of those three, Indiana ranks lowest for both the financial knowledge and education category as well as the financial practices category. Across the seven metrics, Indiana ranks in the bottom five states for its percentage of adults with a three-month emergency fund (44.05%) and percentage of adults paying their credit card bill in full monthly (49.82%).

Data and Methodology

To find the states where Americans are most and least financially literate, we examined data for all 50 states and the District of Columbia across two categories that include seven individual metrics:

- Financial knowledge and education. For our financial knowledge and education index, we analyzed the state’s financial education score, percentage of adults that believe they have a high level of financial knowledge and percentage of correctly answered personal finance quiz questions. The state’s financial education score comes from the Council for Economic Education. Data for the other two metrics comes from the Financial Industry Regulatory Authority (FINRA) Foundation’s 2018 National Financial Capability Study.

- Financial practices. For our financial practices index, we analyzed average credit score, percentage of adults with a three-month emergency fund, percentage of adults paying their credit card bill in full monthly and percentage of adults regularly contributing to an IRA or 401(k). Average credit score figures come from Experian. Data for the other three metrics comes from the Financial Industry Regulatory Authority (FINRA) Foundation’s 2018 National Financial Capability Study.

We created our final rankings by first ranking each state for each individual metric. Then we averaged the rankings across the two categories listed above. For each category, the state with the highest average ranking got a score of 100. The state with the lowest average got a score of 0. Finally, we created our final ranking by finding each state’s average score across the two categories.

The answers to the FINRA Foundation NFCS quiz questions are as follows:

- Mortgage Question – a) True

- Interest Rate Question – a) More than $102

- Inflation Question – c) Less than today

- Risk Question – b) False

- Compound Interest in Debt Question – b) At least two years but less than five years

- Bond Price Question – b) They will fall

Tips for Improving Your Finances

- Take advantage of compound interest. One of the most important things to note about saving is that it helps to start early. Waiting to invest can potentially decrease your total return on a potential investment. Compound interest is interest that’s generated from existing earnings. In other words, when you put money into a savings account earlier, the interest compounds. As a result, you earn interest on the money you initially invested as well as the interest that money has already made. To see how this works, take a look at our investment calculator.

- Some kind of retirement account is better than none. If a 401(k) is not available through your job, consider an IRA. 401(k)s are often valued more than IRAs since there is a possibility that your employer will match your contributions to the plan up to a certain percentage of your salary. This means that if you choose not to contribute, you are essentially leaving money on the table. However, if your employer does not offer a 401(k) plan, an IRA is another great option. In 2020, the IRA contribution limit is $6,000 for people under 50 and $7,000 for people age 50 and older.

- Consider working with a financial advisor. Investing and planning for retirement are complicated and difficult tasks. A financial advisor could help you manage your money smartly. SmartAsset’s free tool matches you with financial advisors in five minutes. If you’re ready to be matched with local advisors that may be able to help you achieve your financial goals, get started now.

Questions about our study? Contact us at press@smartasset.com.

Photo credit: ©iStock.com/Damir Khabirov