While the idea of buying a house may sound fun, the actual securing of a mortgage usually isn’t. Pretty much nobody looks forward to the day they take out a mortgage. Rarely do you hear someone talk about how much they enjoy going through the mortgage process. There’s good reason for this: taking out a mortgage can be a painful, laborious, even depressing endeavor (That’s how little money I have…). All the more incentive to make enough money that you don’t even need a mortgage. Odds are, though, you’re not in that lucky minority. So instead, we’re here to help make the process a little easier. We’ll walk you through the answer to that all-important question, How much mortgage can I afford?

Great to hear because I found my dream home. It costs way more than I make in a year, though.

Well, how much more exactly? Many people will tell you that the rule of thumb is you can afford a mortgage that is two to two-and-a-half times your gross (aka before taxes) annual salary. And some say even higher. There are a ton of variables, and these are just loose guidelines. That said, if you make $200,000 a year, it means you can likely afford a home between $400,000 and $500,000.

Oh, perfect. That was easy. Off to go take out a mortgage now! Bye!

Woah, slow down! We’re just getting started here. Remember? We said this was supposed to be painful, laborious and even depressing. Let’s continue:

There are two things that you need to consider when figuring out the answer to how much mortgage can I afford. First, there’s how much debt you are willing to take on and the second is how much debt a lender is willing to extend to you. The former is definitely important (and we’ll get to that later) but the latter is what we’re going to discuss here.

So we are trying to determine how much your lender thinks you can afford. After all, they’re the one taking the risk by loaning you the money. They’re going to be very concerned about your job, how much money you make in a year, how much money you can put down up front, your credit score and more.

Your lender is going to take all your information and come up with two figures to guide them: your back-end ratio and your front-end ratio.

Never heard of it.

No problem, we’ve got you covered.

The back-end ratio, also referred to as a debt-to-income ratio, is the percentage of your gross annual income (aka income before taxes are taken out) that goes toward paying your outstanding debts. Basically, they want to see how much money you already owe other people before they decide to throw some more money your way. Makes sense, right? They come up with the figure very simply, by dividing your total debt by your total income. The lower the number in this instance, the better. Every lender is going to have a different threshold, but a good ballpark figure is to keep your back-end ratio under 36% for all debt payments, including whatever mortgage you get.

The front-end ratio is also a debt-to-income ratio. But in this case it’s only how much of your income would go toward paying off your mortgage, not counting any other debts. The ratio is calculated by dividing your monthly housing expenses (mortgage payments, mortgage insurance, other various costs) by your monthly income.

OK, so they’ve got my information and done some math. Now what?

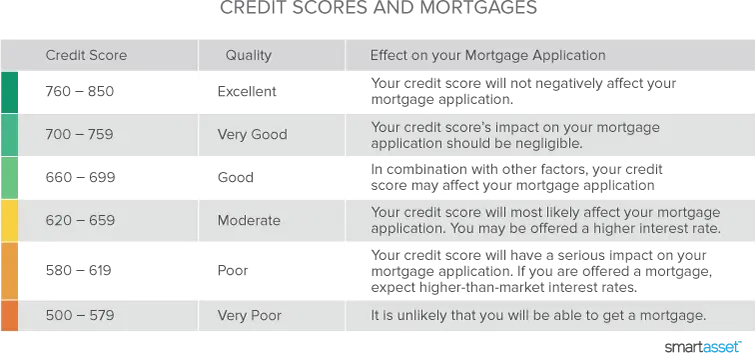

From there, the lender will determine what length of loan and interest rate they feel comfortable giving you. To figure this out, they’ll take a look at your credit score, which ranges from 300 (poor) to 850 (excellent). As you’d expect, the higher your credit score, the lower the interest rate you’ll generally get, though the amount of your down payment also gets factored in.

It’s difficult to say what constitutes an ideal credit score for taking out a mortgage (850 wouldn’t hurt), but a number between 700 and 740 seems to be a good range. In general 620 is considered the lowest acceptable score that will get you the green light.

If your credit score isn’t where you want it, it might be useful to try to boost your number a bit before applying for a mortgage. The difference between a 3-percent and 5-percent rate might not sound huge, but all that interest adds up over the 15 or 30 years of the loan to some pretty significant money.

That makes sense. I think my credit score is in good shape, thankfully. Is there anything else that happens before I get the mortgage?

As far as the lender’s work goes, not really. When determining the answer to How much mortgage can I afford?, the lender can tell you what they’re willing to give you, but it is very important that you take stock of your current situation and assess your future before committing to a loan. In other words, we’re back to the question of what size debt are you comfortable taking on.

What do you mean?

OK, for example, you might be making good money at your current job. But what if you don’t like it and you’re thinking of quitting? And what if your future job doesn’t pay as well and you therefore have less monthly income? Are you going to feel comfortable continuing to pay the same amount each month?

Moreover, how is the health of your parents or your spouse’s parents? Are there medical bills down the road you’re going to have to contend with? Are you thinking of starting or adding to your family?

Basically, you need to be honest with yourself about your personal expenses. How do you like to spend your money? Relatively small things (gym memberships, groceries, etc.) add up and can put a dent in your monthly budget.

You also have to consider how you’re going to decorate the house. Can you afford to furnish every room once you own them? And what do you expect your utility bills to be? What if the stove breaks in six months? Will you have the savings to get it repaired quickly? And speaking of savings, how’s that situation going, or going to change in the months and years ahead? Are you currently trying to stow away lots of money for the future? If so, that’s another issue you need to consider.

One suggestion to figure out at least some of this is to try out your mortgage lifestyle. So once you’ve figured out the answer to the question How much mortgage can I afford?, try actually living as if you are paying that size mortgage for a few months. This can help you figure out if you are really comfortable with that number.

Ugh. This is making my head hurt.

Yup. Mortgages aren’t fun. Still, a house is one of, if not the, most expensive thing you’ll ever spend money on so it’s best to give it a ton of consideration. Being saddled with an unruly mortgage will affect you for years and years. To that end, the more thought you give it now, the less worry you’ll have later. So remember, the question isn’t just How much mortgage can I afford? but How much mortgage do I want? for the long term.