You’ve heard that the two certainties in life are death and taxes? Well, life insurance can help you hedge against both (in a way!). Let’s talk about whether buying a life insurance policy is right for you.

What is life insurance and how does life insurance work?

The history of life insurance goes way back. These days when you purchase a life insurance policy, you start paying to a life insurance company. In return, the life insurance company agrees to pay your beneficiary or beneficiaries a lump sum in the event of your death. There is life insurance for adults, children, veterans, seniors and folks with disabilities. There is term life insurance, limited pay life insurance, cash value life insurance, supplemental life insurance and permanent life insurance. In addition to monetary benefits, the purpose of having life insurance coverage is to give you, the life insurance policy holder, peace of mind. Having it means knowing that your life insurance pay-out will soften the financial blow of your death. So do you need it? Is life insurance worth the cost for you? Here are some questions to consider.

Do you have dependents who need your financial support?

This is the most important question to consider. If you don’t have any dependents, you may be able get away with having no life insurance or buying a smaller policy that will cover your funeral expenses and any unpaid debts you leave behind.

If you’re a parent with children — especially if you’re the only income-earner — life insurance is usually the key financial tool to make sure your family stays afloat if anything happens to you. In general, the younger your kids are, the more money you should have in your life insurance policy. Many parents phase out their life insurance once their kids graduate from college and get off the parental payroll. Others keep some life insurance to ensure their spouse will still be able to lead a comfortable life. Still other people keep life insurance policies to help support parents, siblings or friends who rely on them for financial security. Family life insurance policies can offer discounts for covering more than one member of the same immediate family.

Do you have debt?

When you die with unpaid debt, from credit card bills to mortgages and medical expenses, what you owe usually gets deducted from your estate. Buying a life insurance policy, even if you’re single and childless, can be a smart move if you’re carrying a debt burden. Otherwise, co-signers of loans or joint credit card holders may be responsible for paying back your debt. Life insurance can be an important estate planning tool. It can also be a source of last-resort cash. Some policies allow you to take a life insurance policy loan, borrowing the policy’s cash surrender value.

How old are you?

If you’re in your later years you might not need as much (or any!) life insurance, unless you have young children or a much younger spouse who depends on your earnings and may need your life insurance policy to fund his or her retirement. If you’re young and healthy, life insurance will never be cheaper than it is now, and you can usually lock in low rates. So the answer to the question, Do I need life insurance? may be yes simply because you plan to have a family in the future and want to lock in the lowest possible rate now.

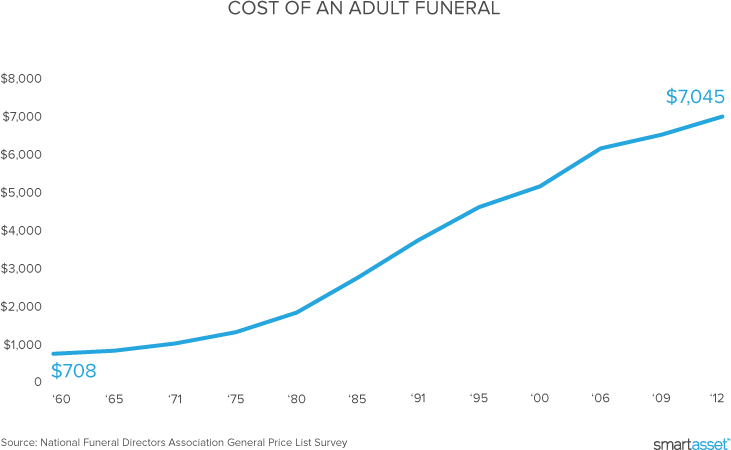

Do you have your heart set on a lavish funeral?

Hey, we’re not judging. Just know that your fancy funeral will cost your loved ones—and plan accordingly. At the very least you should get a life insurance policy that covers final costs like burial expenses. If you only need a small amount of coverage (also known as a low “face amount”), your life insurance premiums should be lower than average. If you can’t afford life insurance premiums, life insurance premium financing (a loan to help you make your premium payments) is an option, but like any loan it carries risks.

How healthy are you?

The less healthy you are, the more dangerous your job and the more diseases run in your family, the greater your need for life insurance is. That’s because the odds are higher that you might leave your dependents in the lurch. Unfortunately, the more you need life insurance for these kinds of reasons, the more you’ll have to pay for it. If you can, you may want to try to get a waiver of premium rider added to your policy. This rider will ensure that your life insurance plan will stay in effect even if you become ill or disabled and can’t keep up with your premiums.

When you buy life insurance, you’re betting that you will die and the insurance company is betting that you won’t. They don’t want you to die, because if you die they have to pay up. So they give the lowest premium rates to the healthiest people with the least dangerous jobs and the most pristine family medical histories. Life insurance premium rates are often divided into different categories, with names like “preferred” and “standard” that correspond to risk levels. If you’re not in the lucky "preferred" category, get ready to pay a little extra for peace of mind for you and your dependents. Unfortunately, life insurance premiums are not tax deductible.

Estate taxing

Once you’ve decided the answer to Do I need life insurance? is 'yes,' and you’ve chosen a beneficiary, start thinking about how to lower the tax burden on your life insurance payout. If possible, you want to keep your policy from being tied up in probate court, and you want to keep estate taxes from eating into the assets your loved ones inherit.

To keep your life insurance policy out of probate court, don’t name your estate as the beneficiary. If you follow this simple rule, the money from your payout will be available quickly when your loved ones need it the most.

If you’re wealthy enough that your estate will be subject to estate taxes, you need to consider how to protect your life insurance policy. The exception to this is if your spouse is your beneficiary, since property left to spouses is not subject to estate taxes. If anyone other than a spouse is your beneficiary and if you are the listed owner of your life insurance policy when you die, the policy will be subject to estate taxes. One strategy for avoiding this scenario is to transfer ownership of the policy to your beneficiary or another trusted adult. Just bear in mind that in doing this, you give up control of the policy and lose the right to change the beneficiary. If you designate someone as an irrevocable beneficiary you will not be able to remove him or her, so it’s important to choose carefully.

Brush up on your Latin

Say you have two sons and you name them both as your beneficiaries, to split the payout equally when you die. Meanwhile, one of them has two daughters and the other has no kids. Now say the son with the two daughters dies before you. When you die, do you A) want half of the payout to go to one son, with the other half split between your two granddaughters? Or do you B) want your son and two granddaughters to split the payout three ways?

If you answered A, you want your life insurance beneficiaries to inherit per stirpes. If you answered B, you want your beneficiaries to inherit per capita.

The… unconventional side of life insurance

When most people think of life insurance, they think of the typical intra-family set-up, where one person takes out a policy to protect children or a spouse. There’s more to the life insurance market, though.

- Life settlements: If you feel you no longer need your life insurance policy or you want to exchange it for money now, you can sell the policy back to the insurance company and redeem the policy’s cash surrender value. Or, you can try to get a higher price for your policy on the secondary market in life settlements. With a life settlement, also known as a viatical, investors pay you more than you would get in cash surrender money from the insurance company, but less than what your beneficiary would get if you died. The investor gets to keep your policy and becomes the beneficiary, and you get ready cash. Not everyone is comfortable with this secondary market, since it’s basically made up of people betting on other people’s death, but it’s perfectly legal.

- Corporate-owned insurance: Another little-known but legal side of the life insurance landscape is corporate-owned insurance, which sometimes goes by the pejorative terms “dead peasant insurance” or “janitors insurance.” With corporate-owned insurance, an employer takes out a life insurance policy on an employee. When the employee dies, instead of the payout going to the worker’s family, it goes to the worker’s boss and into the company coffers. For employers, these plans are tax advantaged and provide a way to hedge against the risk that an employee they’ve invested in won’t be around for the long term.

- STOLI: No, we’re not talking about cheap vodka, we’re talking about stranger-originated life insurance. With a STOLI, an investor asks someone—usually an elderly person—to sell their life insurance policy. Essentially, it’s a life settlement that isn’t the seller’s idea. With a STOLI, a senior gets an offer of easy money. All they have to do is sign some forms authorizing a third party to access their medical records and take over their life insurance policy. The senior takes out a new life insurance policy or transfers an existing policy to an investor they’ve never met before. The investor agrees to pay the premiums on the senior’s policy, and becomes the beneficiary. Usually the senior will get a one-time payment in exchange for his or her trouble. Then, the investor waits for the senior to die and cashes out when the time comes. While these are legal in some states, they are often used as part of less-than-legal scams. In general, the person named as a beneficiary to a life insurance policy should be someone who has what’s called an “insurable interest” in the policyholder. In other words, it must be someone like a spouse, partner, business partner or relative.

One last thing: If you choose to buy life insurance, don’t forget to tell your policy’s beneficiary. Since you’ve decided the answer is yes to do I need life insurance, you really want to know that the money will go where you want it to. Every year, millions of dollars of life insurance policies go unclaimed because the beneficiaries don’t know to claim the money. If you want your policy to go to your loved ones instead of the insurance company (and we’re assuming you do!) don’t keep the policy a secret. Now you just have to answer the question, How much life insurance do I need?