Written by

Written by

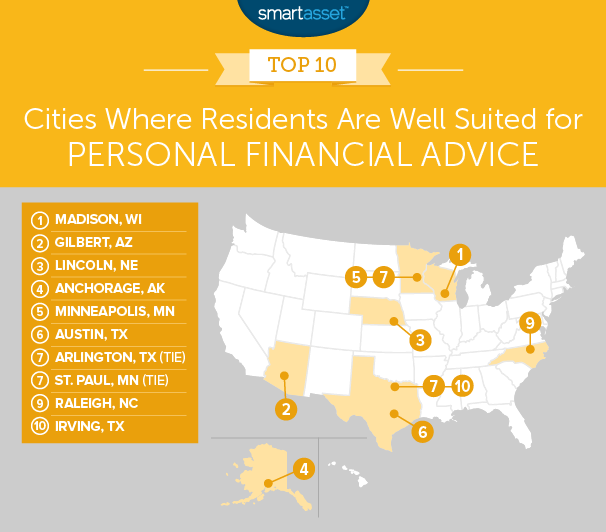

Financial advisors can be a great resource for helping people hit their financial goals, whether they are saving up to buy a home or preparing for retirement. In some cities across the U.S., there are young populations who have high earnings after housing costs who can benefit from professional financial advice. Below we look at these and other factors to rank the cities that are best placed for financial advice.

In order to rank the cities best placed to make the most out of personal financial advice, we looked at data on four factors. We looked at residents’ median age, mean income after housing, percent of households earning more than $75,000 and percent of households that earn over $75,000 and are also housing cost-burdened. Check out our data and methodology to see where we got our data and how we put it together to create our rankings.

Key Findings

- Midwest on top – Midwestern cities occupy three of the top five spots and four of the top 10. The cities have fairly young populations, residents have high incomes and housing is affordable.

- Florida scores poorly – Three Florida cities, Hialeah, Miami and Tampa, all took spots in our bottom 10. These three cities in particular had low average incomes after housing.

1. Madison, Wisconsin

Madison is ranked as No. 1 in this study. It’s a relatively young city with a fairly high income. The median age in this city is 31, making it the eighth-youngest city in terms of population in our analysis.

At the same time these young residents have done well for themselves, income wise. Over a third of households in this city take home more than $75,000 per year. This leaves Madison residents in a good position to invest in their future, which can be maximized by the help of professional financial advice.

2. Gilbert, Arizona

Gilbert, a city within the Phoenix metro area, takes the second spot. It is one of the smallest cities in terms of population in our analysis with only 237,000 residents. Our data suggests Gilbert residents are well-placed to receive financial advice because over half of all households earn more than $75,000 per year. In fact, no other city has a higher proportion of households making over $75,000.

One reason why Gilbert falls behind Madison in our ranking is because, in general, Gilbert households tend to spend slightly more on housing. Around 3.1% of households in Gilbert who earn over $75,000 per year are housing cost-burdened.

3. Lincoln, Nebraska

Nebraska’s capital occupies the third spot. This is a fairly young city with a median age of 32.6. Just under 32% of households earn more than $75,000, a slightly higher-than-average figure.

Those households also do a good job managing their budgets, especially when it comes to housing costs. Less than 1% of the households in Lincoln that earn over $75,000 spend over 30% of their income on housing.

4. Anchorage, Alaska

The mean household income in this city is $105,000 and the median house costs $1,506 per month. That leaves the average Anchorage household with $88,321 after housing costs. For that metric, this city ranks in the top 15.

In Anchorage just over 48% of households have an income over $75,000 per year, a top 10 rate. With these metrics combined, many Anchorage households are in a good place to make long-term investments, whether that be into a 401(k) or the stock market and personal financial advisors can assist with those decisions.

5. Minneapolis, Minnesota

Minnesota’s biggest city comes in fifth. This city ranked in the top half in every metric we tracked. The average household has $67,400 after paying for housing. Of the households in Minneapolis that take home over $75,000 per year, only 1.3% spend over 30% of their income on housing.

That is good news for their investing prospects and for financial advisors in Minneapolis who manage their money.

6. Austin, Texas

Austin households are some of the highest earning in our study. According to our data, the average Austin household has $79,200 after paying for housing. Roughly 36% of households here earn over $75,000. In both of those metrics Austin ranks in the top 20.

7. (tie) Arlington, Texas

Arlington is the second of three Texas cities in this top 10. This city, within the Dallas metro area, contains a relatively young population. The median age of residents in Arlington is 32. Their income after housing is not as high as it is in some of the other cities in our top 10. However, younger people have more time to save, invest and grow their money which may make up for the lower salaries.

According to our data, Arlington households have a mean income of $60,400 after accounting for housing costs.

7. (tie) St. Paul, Minnesota

The eastern portion of the Twin Cities comes in tied for seventh. Residents in this city do a good job keeping their housing costs low. Only 0.8% of residents here who earn over $75,000 spend over 30% of their income on housing. Less money going to housing means households here are in a good place to benefit from personal financial advice.

9. Raleigh, North Carolina

Raleigh is another high-earning city on this list. The mean household income in this city is just over $79,000 and around 35% of households take home over $75,000 per year.

One area where this city could improve its long-term financial prospects is by paying less in housing. According to our data, 1.5% of households earning over $75,000 per year spend over 30% of their income on housing. That metric means less of their income can go to retirement or investments.

10. Irving, Texas

Our list ends in Irving, another city within the Dallas metro area. This city has a median age of 32, 12th-youngest in our study. That leaves the average resident with about 35 years of time to plan and save for retirement. A third of households take home at least $75,000 per year, a number which should mean most households can make great use of personal financial advice.

Data and Methodology

In order to create this ranking, we looked at data for the largest 100 cities in the country. We compared them across the following four metrics:

- Mean income after housing. This is mean household income minus median housing costs.

- Percent of households that earn at least $75,000. This is the percent of households with incomes of $75,000 and higher.

- Percent of households that earn at least $75,000 and are housing cost-burdened. This is the percentage of households earning $75,000 and higher and spend at least 30% of their income on housing costs.

- Median age. This is the median age of each city’s residents.

Data for all metrics comes from the Census Bureau’s 2016 1-Year American Commuity Survey.

First, we ranked each city in each metric. Then we found each city’s average ranking. We assigned out score based on this average ranking. The city with the best average ranking received a 100 and the city with the worst average ranking received a 0.

Tips for Choosing a Financial Advisor

- Certifications matter. Not all personal financial advisors are the same. Depending on your needs you may want to work with a financial advisor who is certified in a specific area. For example a certified public accountant, or CPA, can be helpful for those looking for advice on reducing taxes. A chartered life underwriter, or CLU, would be a fit for someone looking for help with life insurance or estate planning.

- Choose a fee structure that you’re comfortable with. Financial advisors have different payment structures. Fee-only advisors only charge a fee based on a portion of your assets under management. Fee-based advisors charge a portion of assets under management and can also earn commissions for selling you products. Fee-only is a more stringent standard to meet. Some experts will recommend working with fee-only advisors as this leads to fewer conflicts of interest between you and your advisor. Regardless of which payment structure you choose, make sure your financial advisor is a fiduciary. This means they are legally bound to act in your best interests.

- Robo-advisors. A personal financial advisor may not be the best option for everyone. If you are just starting investing, you may not have the minimum amount required to invest with a personal financial advisor. Another option is to use a robo-advisor. A robo-advisor is an online-only advisor that digitally manages your portfolio. Robo-advisors come with lower fees than traditional human advisors. They are a great option for investors looking for a hands-off investing approach.

Questions about our study? Contact us at press@smartasset.com.

Photo credit: ©iStock.com/Rawpixel Ltd