Written by

Written by

The cost differential between renting and buying varies by the amount of time a person expects to stay in a home. Accounting for location, monthly rent and a target home price, SmartAsset’s rent vs. buy calculator determines the amount of time for which buying a home makes more sense than renting. Of course, the amount of time it takes for a renter to save up for the upfront costs of a home is another important consideration. Specifically for people who have their heart set on homeownership, we determined the cities in the U.S. where it takes the least amount of time for renters to become homeowners.

In order to calculate the average time to homeownership in the 100 largest U.S. cities, we used five metrics. They include median income, effective income tax rate, median annual rent, median home value and average closing costs in each city. Using median income, local tax rate and median annual rent, we calculated how much income the average renter would have left over after paying income taxes and rent. We assumed that renters committed to owning one day would be able to save 40% of their post-tax and post-rent income annually, which roughly aligns with the 50-30-20 budget breakdown. We then calculated how long it would take for those savings to cover a 20% down payment and the average closing costs on the median-valued home in each city.

For more information on our data sources and how we put all the information together to create our final rankings, check out our Data and Methodology section below.

Key Findings

- Four years. The average time to homeownership for our top 10 cities is about four years. This is significantly less time than some of the cities at the bottom of our list such as Los Angeles, California and New York, New York. In both of those cities, the estimated time to homeownership is greater than 15 years, almost four times as long.

- Ohio and Texas are great places to save up for buying a home. Six of our top 10 cities where it takes the least time for renters to become homeowners are in Ohio and Texas, split evenly between the two states. They include Toledo, Columbus and Cleveland in Ohio and Irving, Garland and Fort Worth in Texas.

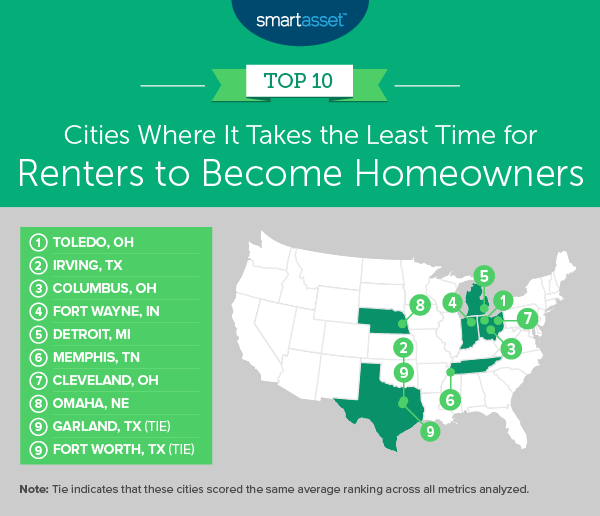

1. Toledo, OH

Of the 100 largest cities in the U.S., the average time to homeownership is the lowest in Toledo, Ohio. According to Census estimates, in 2017, the median income for an individual in Toledo was $26,412, and median annual rent was $8,100. With a tax rate of 11.36% on individuals in that income bracket, renters have an average income of $15,313 after taxes and rent.

For renters looking to buy a home, the median home value in Toledo was only $78,400 in 2017. Assuming a 20% down payment and average closing costs of a little more than $3,000, the upfront costs for buying a middle-priced home in Toledo are about $19,000. Assuming renters are able to save 40% of their post-tax and post-rent income, the amount of time needed to save for the upfront costs of homeownership in Toledo is about three years and one month.

2. Irving, TX

In 2017, the median home value in Irving, Texas was $187,700, the highest amount for this metric of any city in our top 10. Additionally, as Irving is a part of Dallas County, we estimate that closing costs are about $3,475. This means that the combined upfront costs for buying a home in Irving were $41,015 in 2017, also the highest for this metric of any city in our top 10.

While $41,015 is substantial, renters may be able to save up to that amount quickly. We estimate that renters in Irving saving 40% of their income remaining after income taxes and rent may be able to afford the upfront costs of a home in about three years and four months.

3. Columbus, OH

Ohio’s state capital, Columbus, places third on our list. In 2017, the median income in Columbus after taxes and rent was $22,953. Additionally, we estimate that the average upfront costs, including closing costs and a 20% down payment on the median-valued home, for a home in Columbus are about $33,715. Assuming renters save 40% of $22,953, their yearly income remaining after paying taxes and rent, the time to homeownership in Columbus is about three years and eight months.

4. Fort Wayne, IN

According to 2017 Census estimates, the median income for an individual in Fort Wayne, Indiana was $30,225. Additionally, the median home value in Fort Wayne was $117,900 in 2017. Using those median values and assuming that renters save 40% of $17,484, their yearly income after taxes and rent, we estimate that the average time to homeownership in Fort Wayne is about three years and nine months.

5. Detroit, MI

The average upfront costs for a home are the lowest in Detroit, Michigan of any city in our top 10. In 2017, the median home value in Detroit was just $50,200. Assuming a 20% down payment and average closing costs of $4,367, the average upfront costs for a home in Detroit are $14,407. Assuming residents are able to save about $3,700 yearly, which is 40% of the income they have left over after paying for income taxes and rent, the time to homeownership for renters in Detroit is about three years and 10 months.

6. Memphis, TN

Famous for its music scene, Memphis, Tennessee is also an affordable city. It has the fourth-lowest median home value of any city in our top 10 and the fifth-lowest overall of the 100 cities we examined in our study. As a result of home affordability, the time to homeownership for renters in Memphis is relatively short. We estimate that renters will only need to save for a little less than four years on average in order to pay for the upfront costs of a median home.

7. Cleveland, OH

Renters in Cleveland, Ohio may be able to purchase a home in just under four years. In large part, the relatively quick time to homeownership for renters in Cleveland is a product of the low home prices in the city. In 2017, the median home value in Cleveland was the second-lowest of any city in our top 10, at $70,200 – following only Detroit.

8. Omaha, NE

In Omaha, Nebraska, the median income for an individual was $37,778 in 2017. The estimated tax rate on an individual making the above was 14.31%, and median annual rent in the city was $10,704 in 2017. The median home value in Omaha that year was $157,100. We estimate that renters will need to save for just about four years on average in order to pay for the upfront costs of the median home there, which are $34,630 assuming a 20% down payment and average closing costs of $3,210.

9. Garland, TX (tie)

We estimate that the average time to homeownership in Garland, Texas – which ties with Fort Worth, Texas for ninth place in our study – is just over four years. Renters in Garland who are looking to become homeowners would pay upfront costs of $35,815 assuming a 20% down payment and average closing costs of $3,475. The median income for an individual in Garland was $39,179 in 2017, and the median home value that year was $161,700. We estimate that renters could ideally save 40% of their annual post-tax and post-rent income of $22,320 in order to meet this goal.

9. Fort Worth, TX (tie)

Fort Worth, Texas ties with Garland for ninth place in our study. We estimate that the average time to homeownership in Fort Worth is also a little more than four years. Upfront costs for homeowners here are $37,421 assuming average closing costs of $3,541 and a 20% down payment on the median 2017 home value of $169,400. The median income for an individual in Fort Worth that year was $40,324, and the estimated tax rate on that amount was 12.60%.

Data and Methodology

In order to find cities where it takes the least amount of time on average for renters to become homeowners, we looked at five metrics in the largest 100 U.S. cities. They include:

- Median income for an individual. Data comes from the Census Bureau’s 2017 1-year American Community Survey.

- Effective income tax rate. This is the estimated income tax rate for an individual. Data comes from SmartAsset’s income tax calculator using rates from 2017 and applying them to the median income in each city.

- Median annual rent. Data comes from the Census Bureau’s 2017 1-year American Community Survey.

- Median home value. Data comes from the Census Bureau’s 2017 1-year American Community Survey.

- Average closing costs. Data is from SmartAsset’s closing costs calculator and is calculated on the county-level.

Using median income, local tax rate and median annual rent, we calculated income after taxes and rent in each place. We assumed that renters committed to owning one day would be able to save 40% of this post-tax and post-rent income annually, which roughly aligns with the 50-30-20 budget breakdown. Then, using median home value and average closing costs, we calculated the upfront costs for a home. We divided the upfront costs for a home by 40% of post-tax and post-rent income amount in order to find the average amount of time to homeownership for a renter in each city.

Tips for Managing Your Savings

- Invest early. An early retirement requires early planning. By planning and saving early, you can take advantage of compound interest. Take a look at our investment calculator to see how your investments can grow over time.

- Buy or rent? – When you’re moving to a new city, you need to decide if you are going to rent or buy. Speaking to a financial advisor may help you make that decision more easily. Finding the right financial advisor that fits your needs doesn’t have to be hard. SmartAsset’s free tool matches you with financial advisors in your area in 5 minutes. If you’re ready to be matched with local advisors that will help you achieve your financial goals, get started now.

Questions about our study? Contact us at press@smartasset.com

Photo credit: ©iStock.com/LaylaBird