Written by

Written by  Edited by

Edited by  Edited by

Edited by  Reviewed by

Reviewed by

Vanguard and Fidelity are both major brokerage firms, with some of the largest client bases in the country. Each has broad financial offerings, from DIY brokerage accounts to financial advisors, robo-advisors and financial planning services. Vanguard is also widely known for its in-house selection of low-cost funds, as it runs a number of its own indexes. On the other hand, Fidelity offers in-depth investment tools that are great for veteran investors looking for the upper hand. Each option has its own strengths and weaknesses in terms of its fees, online experience and features.

If you need help with your finances, consider using SmartAsset’s free advisor matching tool to find a fiduciary financial advisor who serves your area.

Vanguard vs. Fidelity: An Overview

There aren’t many bigger names in the brokerage space than Vanguard and Fidelity. They consistently boast some of the largest client bases in the country, and for good reason. Both brokerages have extensive investing tools and platforms that make managing your investments and financial plans much easier.

Vanguard has long been known for its wide range of in-house index funds and exchange-traded funds (ETFs). If you’re looking to invest in funds, going directly to a main provider like Vanguard can significantly lower your costs. That’s because Vanguard can afford to offer lower expense ratios than other brokerages that allow you to invest in third-party funds.

While Vanguard stands out with its suite of funds, the brokerage is more limited when it comes to other offerings. However, it does allow investors to trade individual stocks and bonds. Conversely, Fidelity allows clients to invest in individual stocks, bonds, ETFs, options, mutual funds and more.

Vanguard vs. Fidelity: Fees

| Fee Type | Vanguard | Fidelity |

|---|---|---|

| Investment Fees | – Stocks and ETFs: $0 online – Vanguard mutual funds: $0 online – Non-Vanguard no-transaction-fee mutual funds: $0 online – Non-Vanguard transaction-fee mutual funds: $20 online for clients with less than $1 million in qualifying assets, with waivers or lower fees available at higher asset levels – Options: $0 commission and $1 per contract, with limited commission-free trades for eligible clients – New-issue CDs, U.S. government agency securities, corporate bonds and U.S. Treasuries: $0 – Secondary-market CDs, U.S. government agency securities and corporate bonds: $1 per $1,000 of face amount, up to $250 per transaction – Secondary-market U.S. Treasuries: $0 – Secondary-market municipal bonds: $1 per $1,000 of face value, up to $250 per transaction – Mortgage-backed securities: $35 per trade | – Stocks & ETFs: $0 online – Fidelity mutual funds: $0 No-transaction-fee non-Fidelity mutual funds: $0 on purchase, with a $49.95 redemption fee if held for less than 60 days – Transaction-fee non-Fidelity mutual funds: $49.95 per purchase, with certain funds costing up to $100 – Options: $0 commission and $0.65 per contract – New-issue bonds: $0 – Secondary-market bonds and CDs: $1 per bond – Online U.S. Treasury auctions and secondary-market U.S. Treasuries: $0 |

| Account Fees | – Account fee: $25 a year (waivable) – Wire transfer fee: $10 – Foreign securities transactions: $50 | – Account fee: $0 – Domestic wire transfer fee: $0 – Foreign exchange wire transfer fee: Up to 3% of principal – Foreign securities transactions: $50 |

Fees are important to consider when picking a brokerage firm to open an account with. You’ll want to make sure that the fees are fair and within your budget, as an overbearing fee structure will have a large negative effect on your portfolio.

A commission-lowering wave has struck brokerage firms over the last couple of years, and Fidelity and Vanguard have both followed suit. To trade stocks, ETFs, options and many mutual funds, clients of both firms will avoid commissions altogether. Options at Vanguard come with a $1 contract fee, while Fidelity charges an even lower $0.65 contract fee.

For secondary-market bonds and CDs, Fidelity charges $1 per bond or CD, as well as a minimum $19.95 markup or markdown if you initiate a representative-assisted transaction. Vanguard doesn’t charge fees for new-issue CDs, U.S. government agency securities, corporate bonds or U.S. Treasuries, but its secondary-market CDs, agency securities, corporate bonds and municipal bonds come with a $1 per $1,000 face amount fee, up to $250 per transaction, plus a $25 broker-assisted fee if purchased over the phone by clients with less than $1 million in qualifying assets.

In regard to account fees, Vanguard may charge a $25 annual account service fee. On the other hand, Fidelity doesn’t charge an account fee for retail brokerage accounts, including IRAs. Vanguard has a few ways to waive this fee, including holding at least $1 million in qualifying assets, electing e-delivery or having an organization or trust account with a registered EIN.

Vanguard vs. Fidelity: Features

Investment Products

Both Fidelity and Vanguard offer a variety of investment products, including proprietary mutual funds and ETFs.

Vanguard specializes in low-cost, passively managed index funds and ETFs, making it an attractive option for buy-and-hold investors. Its product lineup includes popular funds like the Vanguard Total Stock Market ETF (VTI) and Vanguard 500 Index Fund (VFIAX). Fidelity, on the other hand, offers a broader array of actively managed funds alongside its passively managed options. Fidelity’s ZERO index funds, such as the Fidelity ZERO Total Market Index Fund (FZROX), are particularly notable for their lack of expense ratios.

Account and Fund Minimums

Additionally, Fidelity has $0 account minimums for retail brokerage accounts and no investment minimums for Fidelity mutual funds. While Vanguard also has a $0 account minimum, the company often has fund minimums. For its Investor Shares, the minimums range from $1,000 to $3,000, depending on the fund.

However, the company notes that most of its index funds no longer offer Investor Shares to new investors. Meanwhile, Admiral Shares generally require $3,000 for most index funds, $50,000 for most actively managed funds and $100,000 for certain sector-specific index funds. Investors must meet and maintain the applicable minimum to qualify for Admiral Shares.

When it comes to investment options, both firms have offerings that may be suitable for your portfolio. If you’re unsure which firm has funds that meet your budget and investment objectives, you can compare funds by using each broker’s fund screener.

Trading Tools

Fidelity and Vanguard both offer robo-advisor services, educational tools and mobile apps to help you better manage your money. However, for those who want to actively trade, Fidelity offers Fidelity Trader+ Desktop, previously known as Active Trader Pro. This service helps investors stream data and customize charting. Vanguard doesn’t have a similar service.

Vanguard Personal Advisor

For people who want investment advice, Vanguard offers a hybrid robo-advisor service called Vanguard Personal Advisor. This service uses algorithms to help with portfolio construction and asset allocation. It also offers human advisors who can answer financial planning questions and concerns via phone or online. Vanguard requires a minimum $50,000 account for this service and charges a 0.30%-0.31% annual management fee.

Vanguard Personal Advisor Select

Vanguard also offers its Personal Advisor Select program for those with higher net worth. In fact, the minimum for this service is $500,000, though its maximum annual advisory fee is 0.30%. This is a more in-depth offering than the base Personal Advisor program, though Vanguard also offers Personal Advisor Wealth Management for investors with at least $5 million in Vanguard funds and ETFs. Personal Advisor Select pairs you with a dedicated advisor at the company. This will allow you to build a relationship with a dedicated Certified Financial Planner™ (CFP®), as opposed to having various professionals work with you in the base program.

Vanguard Digital Advisor

However, if you don’t have enough money to invest in Vanguard’s Personal Advisor services, it also offers Vanguard Digital Advisor. This program is a bit more basic than its counterpart, but it requires just a $100 minimum investment in a Vanguard brokerage account. Fees are nonexistent for your first 90 days as a client. Once that period ends, you’ll pay an annual gross advisory fee of 0.20% for an index portfolio or 0.25% for an active portfolio. Vanguard applies revenue credits that reduce the actual net advisory fee collected.

Fidelity Go

Fidelity also offers one robo-advisor service called Fidelity Go. This platform is designed for investors who want Fidelity to manage their portfolio. Clients with at least $25,000 receive access to unlimited one-on-one financial coaching calls with a team of Fidelity advisors. Taxable accounts with at least $25,000 also receive tax-loss harvesting. There is no minimum to open a Fidelity Go account, though the balance must reach $10 before Fidelity begins investing the money. There is no annual fee if your account balance is less than $25,000. For accounts with a balance of $25,000 or more, there’s a 0.35% annual fee.

Vanguard vs. Fidelity: Environmental, Social and Governance Issues

Both brokerages highlight their commitment to environmental, social and governance (ESG) issues by making mutual and exchange-traded funds (ETFs) available to clients. Fidelity offers a long list of funds whose managers consider ESG priorities as they build and maintain portfolios. Vanguard offers ESG funds that are indexed and follow an exclusionary strategy that omits companies that don’t meet certain ESG criteria. The brokerage firm also has three active funds that invest in companies with leading or improving ESG practices.

At the same time, both firms have elected to either withdraw from or not affiliate with prominent ESG associations. In December 2022, Vanguard withdrew from the Net Zero Asset Managers Initiative (NZAM), an alliance of asset managers committed to supporting net-zero greenhouse gas emissions by 2050 or sooner. Also in late 2022, Fidelity joined other major financial institutions in choosing not to affiliate with the Glasgow Financial Alliance for Net Zero.

Vanguard vs. Fidelity: Advisory Services

Both firms offer the services of financial advisors. These are designed for those who want the firms’ highest-level packages, as you’ll get to work with an advisor in a hands-on manner. Vanguard charges fees for its advisory services that are tailored to each client. The fee rate can vary depending on the complexity and size of the account, and the frequency at which clients pay will be specified in the initial advisory agreement.

The firm’s offshore clients will also have to pay various administrative and operational expenses that aren’t included in the standard advisory fees. Vanguard doesn’t charge performance-based fees, so clients’ fees are not dependent on capital gains or asset appreciation.

The minimum for Fidelity’s advisory services begins at $50,000, which makes it readily accessible to investors of modest means. However, the firm also offers digital, discretionary investment management services with no minimum requirement and personalized planning advice for a $25,000 minimum. For its private wealth management services, Fidelity requires clients to invest at least $2 million in investable assets.

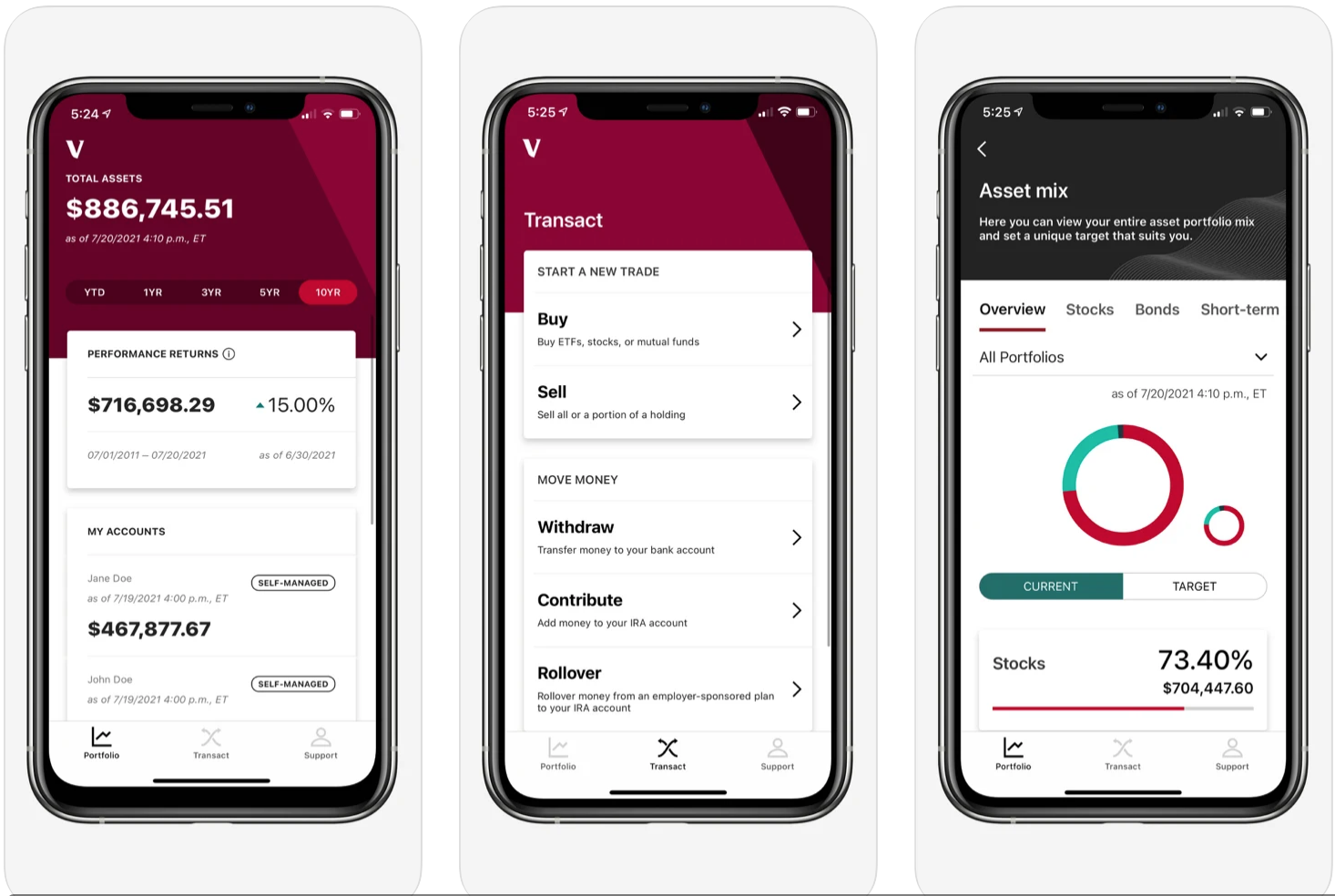

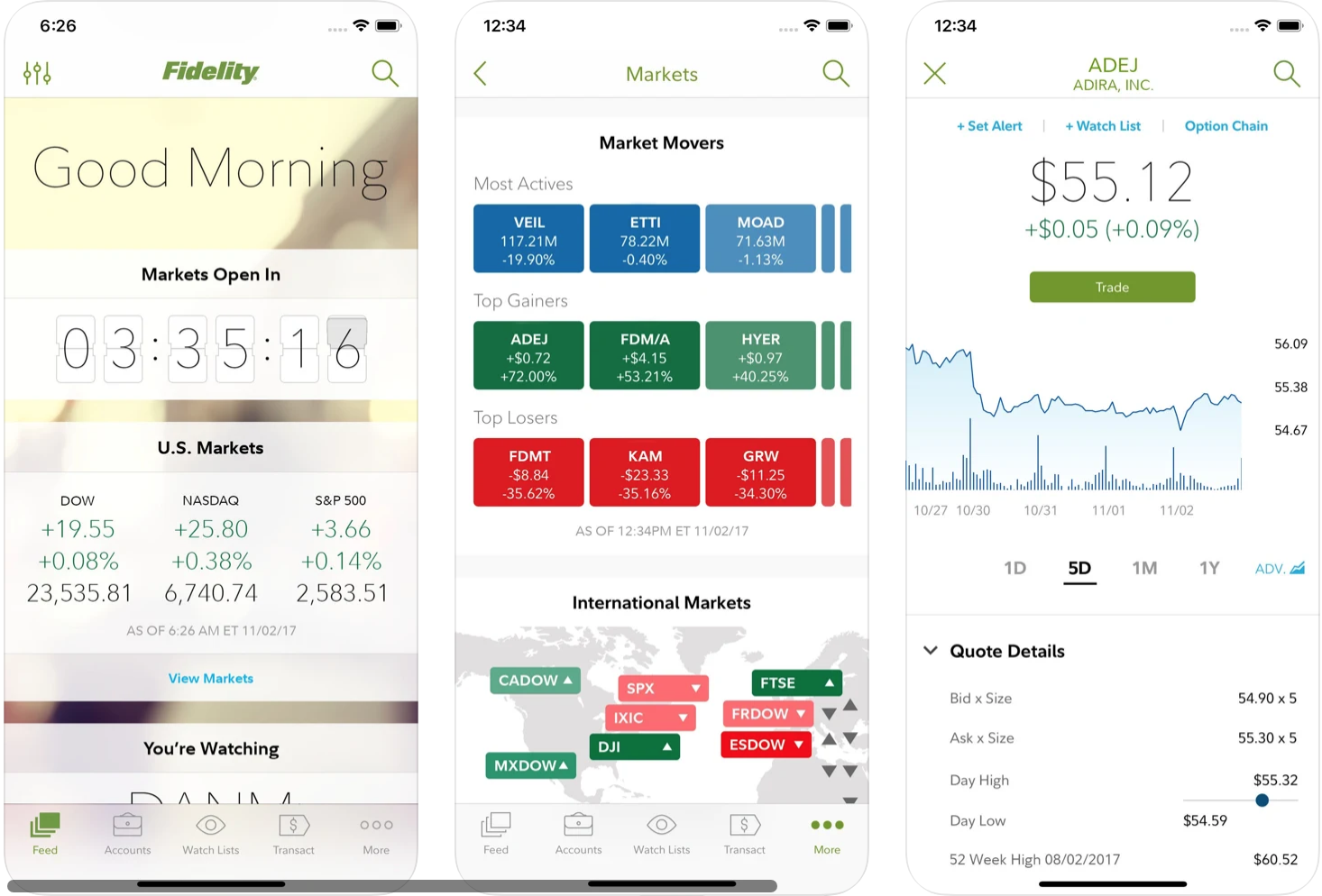

Vanguard vs. Fidelity: Online and Mobile Experience

Both brokerages have robust online and mobile experiences. So while each firm has features and investments that favor specific types of clients, the quality of their tools and platforms is unquestionably strong.

Vanguard’s trading platform and apps are fairly basic, in keeping with the general aesthetic of the company. You can do everything you need to do as a retail investor: make trades, buy mutual funds and check your performance. The platforms don’t have all the bells and whistles an experienced investor might want, but for someone who just wants to manage a few basic investments, it works.

Fidelity, on the other hand, has a more complicated and extensive online and mobile experience. While this may be a bit overwhelming for someone without a ton of investing experience, if you have been trading for a while, Fidelity may help you take your investing game to the next level.

As of July 2026, Vanguard’s mobile app has a significant variance in its satisfaction level among users. For the Apple version, users rate it at 4.6 stars out of 5 across over 177,000 reviews. But on the Google Play store, Android users rate it at just 2.7 stars out of 5 across more than 11,000 reviews.

Fidelity’s mobile app has a higher level of user approval than Vanguard’s. The app has an average rating of 4.8 stars out of 5 across more than 3.2 million iPhone ratings. The app also holds a respectable 4.1 stars out of 5 rating on the Google Play store across more than 218,000 reviews.

Who Should Use Vanguard?

Vanguard built a reputation as a platform that creates and offers low-fee mutual funds and exchange-traded funds. This makes it a good brokerage for clients who want to make basic investments and not think too much about them. In addition, if you want low-cost funds, Vanguard has also grown to offer stocks and bonds. However, trading these individual equities is much more limited.

Vanguard might also make sense for clients who want to open an IRA and manage it in a very hands-off manner. At its core, the brokerage is designed for investors who want a simple experience. Its accounts and tools are easy to use, and its website boasts several educational resources. This makes it extremely welcoming to beginners.

Who Should Use Fidelity?

Fidelity is a robust trading platform that is known for its individual trading products, which include stocks and bonds. Most clients would be happy with Fidelity, but it is especially suited for those with ample investing experience. Its advanced investment tools and platforms can be overwhelming if you’re a newbie. Beyond that, if you’re going to be making frequent trades, Fidelity could be a good choice.

While Fidelity does not charge much for its investment resources, it is also worth noting that other brokerages and broker-dealers are shifting to fee-free investment models. Keeping this in mind, you’d be hard-pressed to find a better selection of high-level tools at an established brokerage. Many competitors have smaller pools of potential investments and less overall reliability than Fidelity.

Bottom Line

If you want to actively trade within your accounts, Fidelity might be the better option. However, if you want to focus more on index investing, or you want to use a robo-advisor, Vanguard has a slight edge. While both institutions offer robo-advisors, Vanguard’s Personal Advisor Services, which is available to clients who can meet a $50,000 account minimum, offers a little more hands-on investment guidance and assistance with portfolio construction. Vanguard also has slightly lower expense ratios on its index funds.

If you want help with financial planning, mutual funds or retirement and brokerage accounts, both have great options. It’s best to compare each firm’s costs, minimum account requirements and fund selection. By comparing your options, you can discover the most suitable firm for your financial needs.

Tips for Investors

- Both Vanguard and Fidelity are attractive brokerages for retail investors, but there can still be great value in also working with a financial professional. Finding a financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with vetted financial advisors who serve your area, and you can have a free introductory call with your advisor matches to decide which one you feel is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

- If you decide to go with a brokerage, SmartAsset can recommend a few online options. Once you’ve considered the above factors and compared online brokerages, you’ll be in a position to find the right choice for you.

Photo credit: ©Vanguard/Fidelity, ©iStock.com/DNY59, ©Vanguard Beacon Apple Store Preview, ©Fidelity Investments Apple Store Preview, ©iStock.com/izusek