Written by

Written by

Though the COVID-19 pandemic has financially impacted Americans in many ways, the homeownership rate has risen and stayed elevated. Census Bureau data shows that the homeownership rate actually hit 67.9% in the second quarter of 2020, up from 64.1% from a year before. More recently, the national homeownership rate was 65.4% in the second quarter of 2021, which is slightly higher than pre-COVID-19 rates.

Though rates are rising by and large, homeownership remains more achievable in some places than others. In this study, SmartAsset examined how long it takes for renters to become homeowners in the 100 largest U.S. cities. We also consider the estimated time to homeownership in the 15 largest U.S. cities, accounting for either a 10% or 20% down payment on the median valued home in each place. Check out our Data and Methodology section below to see where our data comes from and how we calculated time to homeownership estimates.

This is SmartAsset’s second annual study on how long it takes to become a homeowner in U.S. cities. Check out the 2020 edition here.

Key Findings

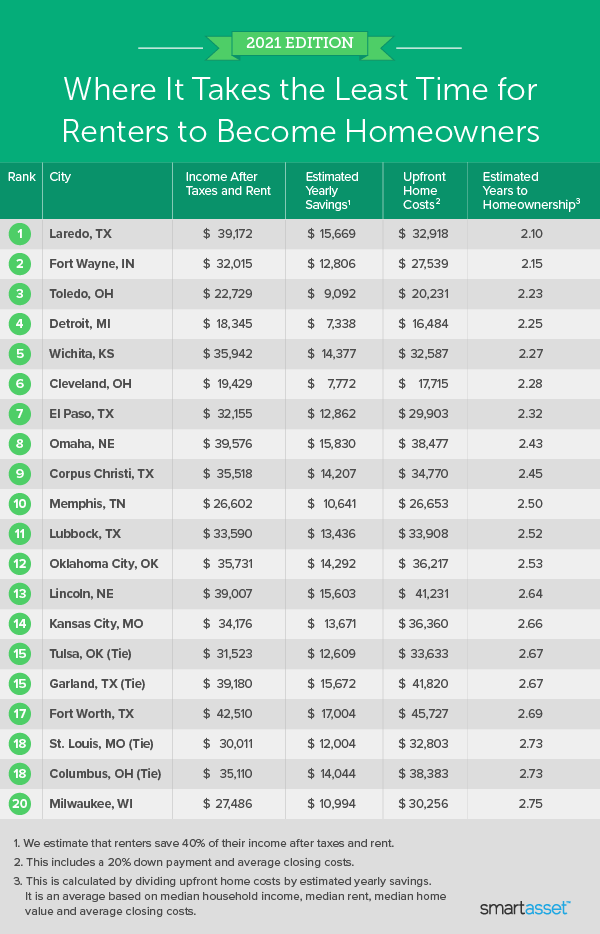

- Midwest cities dominate the top 10. Six of the 10 cities where it takes the least time for renters to become homeowners are in the Midwest. They include Fort Wayne, Indiana; Toledo, Ohio; Detroit, Michigan; Wichita, Kansas; Cleveland, Ohio and Omaha, Nebraska. The estimated average length of time for renters to become homeowners in all six of those cities is less than two and a half years.

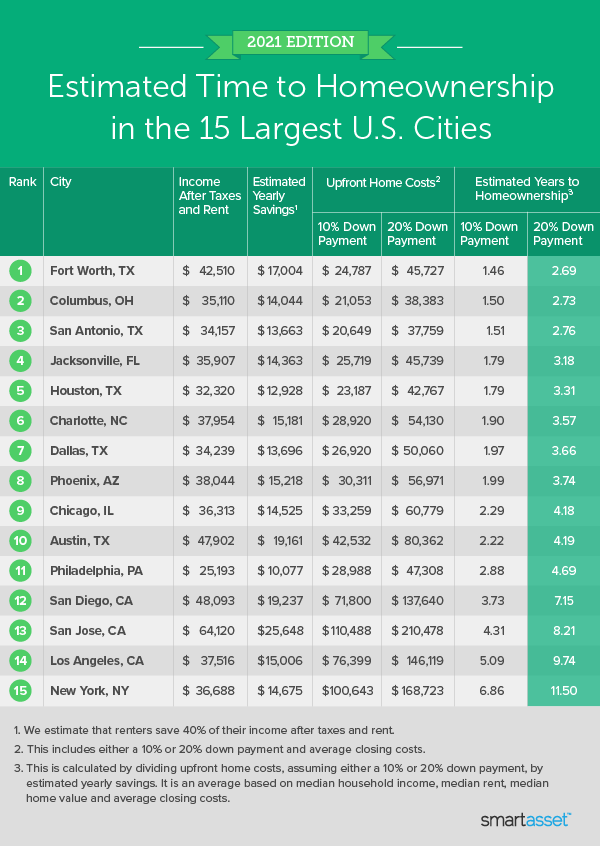

- Homeownership may be the most elusive for New Yorkers. The estimated time for renters to become homeowners is longest for people living in New York, New York. We found that it may take upwards of 11 years for renters in the Big Apple to save enough to afford a 20% down payment and closing costs. Even people planning to put only 10% down on a home or apartment may need to save for upwards of six years.

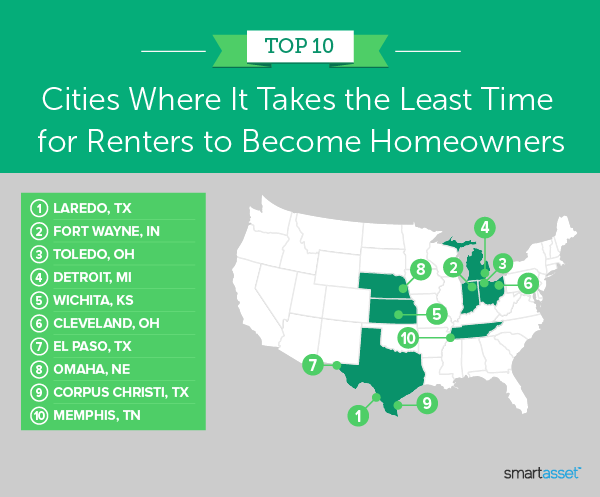

Cities Where It Takes the Least Time for Renters to Become Homeowners

To calculate the average time to homeownership in the 100 largest U.S. cities, we looked at five metrics. They include median household income, effective income tax rate, median annual rent, median home value and average closing costs. Using income, tax rates and rent figures, we calculated income after taxes and rent in each city. We assumed renters would be able to save 40% of their post-tax and rent income annually. We divided the upfront costs for a home, including a 20% down payment on the median-valued home and average closing costs, by that savings figure to estimate an average length of time for renters to become homeowners.

1. Laredo, TX

With the lowest average time to homeownership, Laredo, Texas ranks as the No. 1 city in our study. Census data shows that the median household income in Laredo is about $57,500. After taxes and rent, the average household has about $39,200 leftover in disposable income. Assuming 40% of this figure is saved annually, renters may be able to afford a home in close to two years.

2. Fort Wayne, IN

The median household income in Fort Wayne, Indiana is almost $49,900, and the median home value here is $124,400. Using those figures, we found that the average household in the city may be able to afford the upfront costs for a median valued home in 2.15 years.

3. Toledo, OH

Renters in Toledo, Ohio may be able to purchase a home in just under two years and three months. A 20% down payment on the median valued home in Toledo is about $16,900. With average closing costs at about $3,300, a household needs roughly a total of $20,200 to put down on a home.

4. Detroit, MI

Like last year, Detroit has the lowest median home value ($58,900) of any city in our top 10. With this low average home cost, renters may be able to afford the upfront costs of homeownership more quickly. We estimate that the average time to homeownership for renters in Detroit is 2.25 years.

5. Wichita, KS

Using Census Bureau data along with our income tax calculator, we found that the average household in Wichita, Kansas may be able to save about $14,400 annually. Assuming average upfront home costs of roughly $32,600, the estimated time to homeownership is 2.27 years.

6. Cleveland, OH

Cleveland, Ohio moves up this year from its No. 8 spot in 2020, with the estimated time to homeownership dropping from 2.43 years to 2.28 years. This change is primarily due to an increase in the median household income. According to Census Bureau data, the median household income rose by about 7% from 2018 to 2019. As a result, renters may be able to save more each year, making homeownership possible sooner.

7. El Paso, TX

El Paso, Texas ranks seventh in our study. The median household income in El Paso is about $48,500, and the median home value here is $133,600. Using those figures, we found that renters may be able to afford the upfront costs for a median valued home in the city in 2.32 years.

8. Omaha, NE

Census estimates show that the median household income in Omaha, Nebraska is about $61,300. Additionally, the median home value is $175,800. Using those figures along with the previously described methodology, we estimate that the average time to homeownership in Omaha is less than two and a half years.

9. Corpus Christi, TX

Corpus Christi is the last of three Texas cities that rank in our top 10 cities where it takes the least time for renters to become homeowners. With Corpus Christi’s relatively affordable rent, the average renters here may be able to save upwards of $14,200 annually. This means that they may be able to afford the upfront costs of a home – roughly $34,800 – in 2.45 years.

10. Memphis, TN

Memphis, Tennessee rounds out our list of the top 10 cities where it takes the least time for renters to become homeowners. A 20% down payment on the median valued home in Memphis is about $23,200. With average closing costs at roughly $3,500, a household needs approximately a total of $26,700 to put down on a home at the time of purchase.

Estimated Time to Homeownership in the 15 Largest U.S. Cities

In addition to examining the cities where it takes the least time for renters to become homeowners, we took a closer look at the estimated time to homeownership in the 15 largest cities in the U.S. Because not everyone puts down 20% on a home, we explored time to homeownership scenarios for putting 10% down and 20% down on the median home value.

Across the 15 largest cities, Fort Worth, Texas has the lowest estimated time to homeownership. The average household in Fort Worth could afford the upfront costs of buying a home in 2.69 years if they put 20% down on a house, or 1.46 years if they put 10% down on a house.

Columbus, Ohio ranks second, moving down one spot from last year. Average upfront home costs in Columbus are about $38,400 for a 20% down payment and closing costs or roughly $21,100 for a 10% down payment and closing costs. The table below shows how the 15 largest U.S. cities stack up.

Data and Methodology

To find cities where it takes the least average time for renters to become homeowners, we considered five metrics. They include:

- Median household income. Data comes from the Census Bureau’s 2019 1-year American Community Survey.

- Effective income tax rate. Data comes from SmartAsset’s income tax calculator.

- Median annual rent. Data comes from the Census Bureau’s 2019 1-year American Community Survey.

- Median home value. Data comes from the Census Bureau’s 2019 1-year American Community Survey.

- Average closing costs. Data is from SmartAsset’s closing costs calculator and is calculated on the county level.

Using median household income, effective income tax rate and median annual rent, we calculated income after taxes and rent in each city. We assumed households renting would be able to save 40% of their post-tax and rent income annually. Then, using median home value and average closing costs, we calculated the upfront costs for a home. We divided the upfront costs for a home by 40% of post-tax and rent income to find the average amount of time to homeownership for a renter in each city.

Home-Buying Tips

- Mortgage management. It is important to know when purchasing a home what you’ll be paying each month and for how long. To get a sense of what that might look like, check out SmartAsset’s free mortgage calculator.

- Buy or rent? Even if you have the savings to buy a first home, be sure the switch makes sense. If you are coming to a city and plan to stay for the long haul, buying may be the better option for you. On the other hand, if your stop in a new city will be a short one, you’ll likely want to rent. SmartAsset’s rent vs. buy calculator can help you see the cost differential between purchasing a home or apartment and renting.

- Seek out trusted advice. No matter where you live, a financial advisor can help you get your financial life in order. SmartAsset’s free tool matches you with up to three financial advisors in your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor, get started now.

Questions about our study? Contact us at press@smartasset.com.

Photo credit: ©iStock.com/monkeybusinessimages