Even if your wedding was all about eternal love, companionship and mason jars wrapped in twine, don’t fool yourself: at the end of the day, your marriage is essentially a tax arrangement in the eyes of the state.

When two people become one unit, the way they pay into our society changes, as their income, investments and property starts being viewed differently by the powers that be. Whether or not your marriage works out in your favor or not financially, though, could depend on how much money each individual makes and where you live.

A trusted financial advisor can help you be strategic about your finances and explore ways to lower your tax liabilities. If you’d like to match with a financial advisor in your area, get started here.

The federal government, along with many state governments and some local governments, has a system of progressive tax rates whereby marginal tax rates increase as a taxpayer’s income increases. Because of this system, a couple’s income can be taxed either more than or less than that of a single filer’s, causing a marriage tax penalty or bonus.

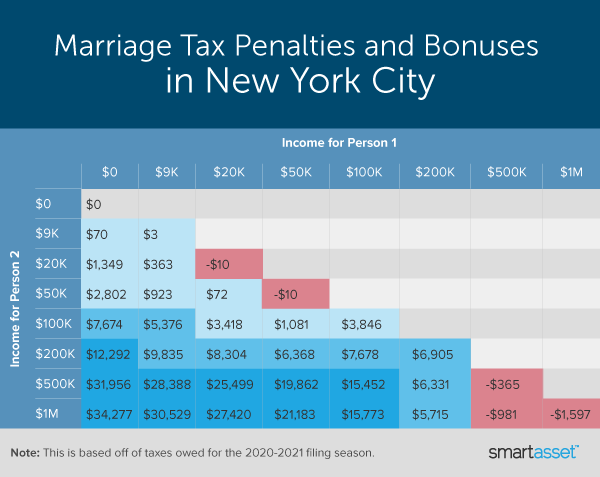

To see this in action, let’s consider a couple living in New York City where both the city and state also have a progressive tax system. The table below shows the marriage tax penalties and bonuses for couples with incomes that span the seven federal tax brackets.

Suppose one person earns $100,000 annually while the other earns $50,000. When single, the first partner will be taxed a total of $31,572, an effective tax rate of 31.57%. The second, lower-earning partner has a total tax bill of $11,944, or an effective tax rate of 23.89%. In total, the unmarried couple owes $43,516 in taxes.

Now, though, let’s say the two get married. The total federal income tax for the two filing jointly will be $42,435, an effective tax rate of 28.29%. Thus, the federal marriage bonus for this couple is about $1,100.

While progressive tax rates often benefit individuals with greater income gaps who get married, they sometimes penalize couples who earn roughly the same. At the federal level, a marriage penalty only occurs for high earners. When taking state and local taxes into account, though, there can be a penalty for lower-income earners as well.

Let’s consider a second couple living in New York City. Suppose both individuals earn $500,000 annually. When they file separately, each has an income tax bill of $215,122 — a total tax bill of $430,244 between the two of them, or an effective rate of 43.02%. Married, their total tax bill is slightly higher, at $430,609.

Finally, let’s look at a couple in New York City each earning $50,000. Separately, each owes a total of $11,944. Combined, that’s $23,888, an effective tax rate of 23.89%. If these two get married, they will owe $23,898, an effective tax rate of 23.90%. That comes to a small marriage penalty of $10.

Bottom Line

As a general rule, marriage provides a modest bonus in the form of lower effective tax rates, with greater bonuses when there’s a significant disparity in incomes. Still, at some higher income levels, getting married to someone with similar earning power can mean higher tax rates. Consider using our tax calculator to see the before and after of your own marriage – or, if your financial picture is more complicated, consider working with a financial advisor who can help you understand the financial implications of getting hitched.

Tips for Maximizing Your Tax Savings

- Estimate your income taxes. Many of the scenarios above may not apply to your unique financial situation. To get a better look at what kind of taxes you will pay as an individual versus if you file jointly with a partner, check out our income tax calculator. By adding your and your partner’s information separately and jointly, you can see how marriage may affect your overall tax situation.

- Be smart about how you file. The above study focuses specifically on the case in which a married couple files jointly. However, the IRS gives married couples two different tax filing status options: married filing jointly and married filing separately. While filing jointly as a married couple may lead to a tax bonus and other benefits such as qualifying for additional tax credits, filing separately may be the right decision for you and your partner. If you are weighing the pros and cons, take a look at our guide: 3 Reasons Married Couples Should Consider Filing Taxes Separately.

- Go beyond taxes to build a comprehensive financial plan. A financial advisor can help you make smarter financial decisions to be in better control of your money. Finding the right financial advisor who fits your needs doesn’t have to be hard. SmartAsset’s free tool matches you with financial advisors in your area in five minutes. If you’re ready to be matched with local advisors that will help you achieve your financial goals, get started now.